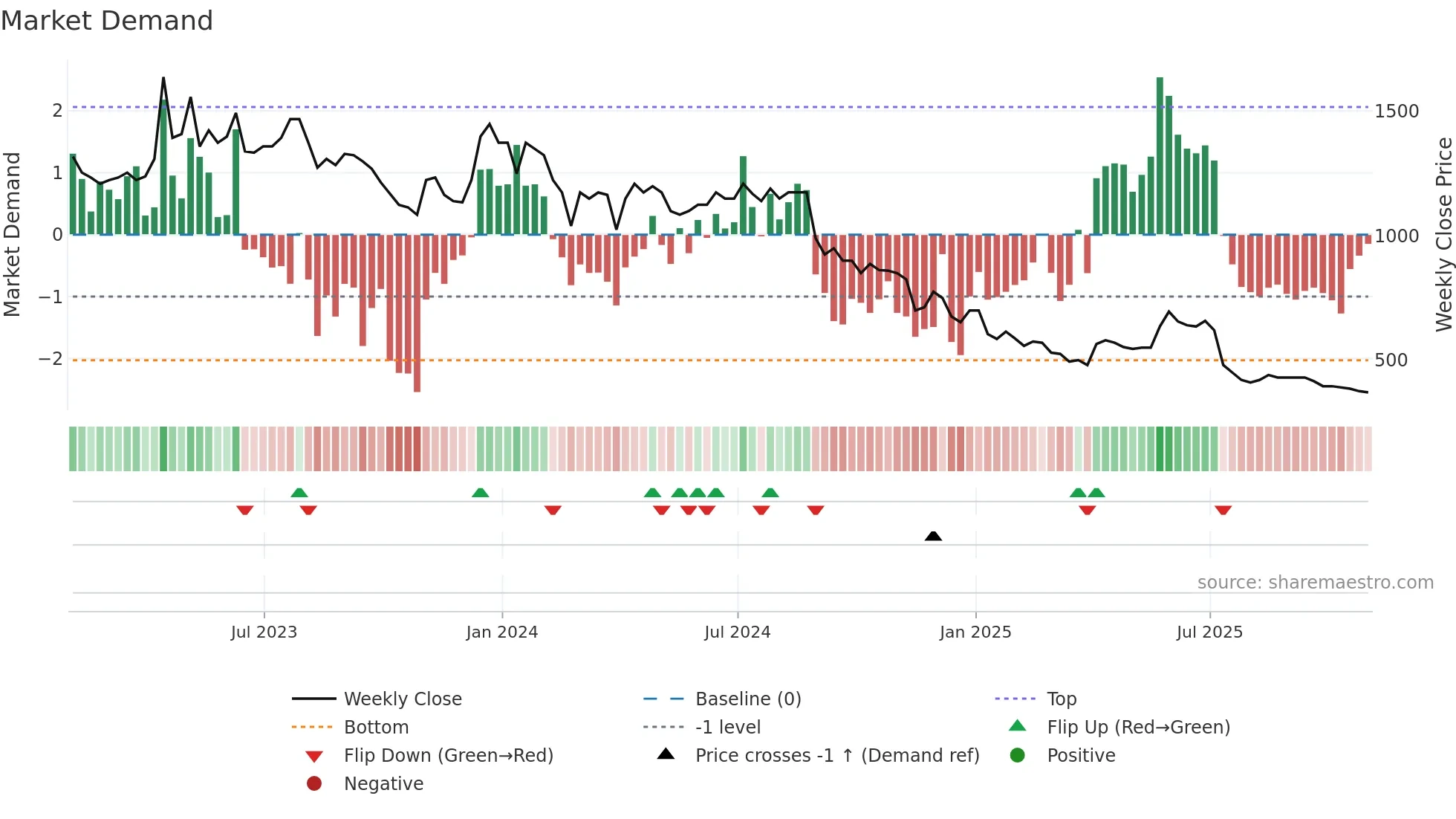

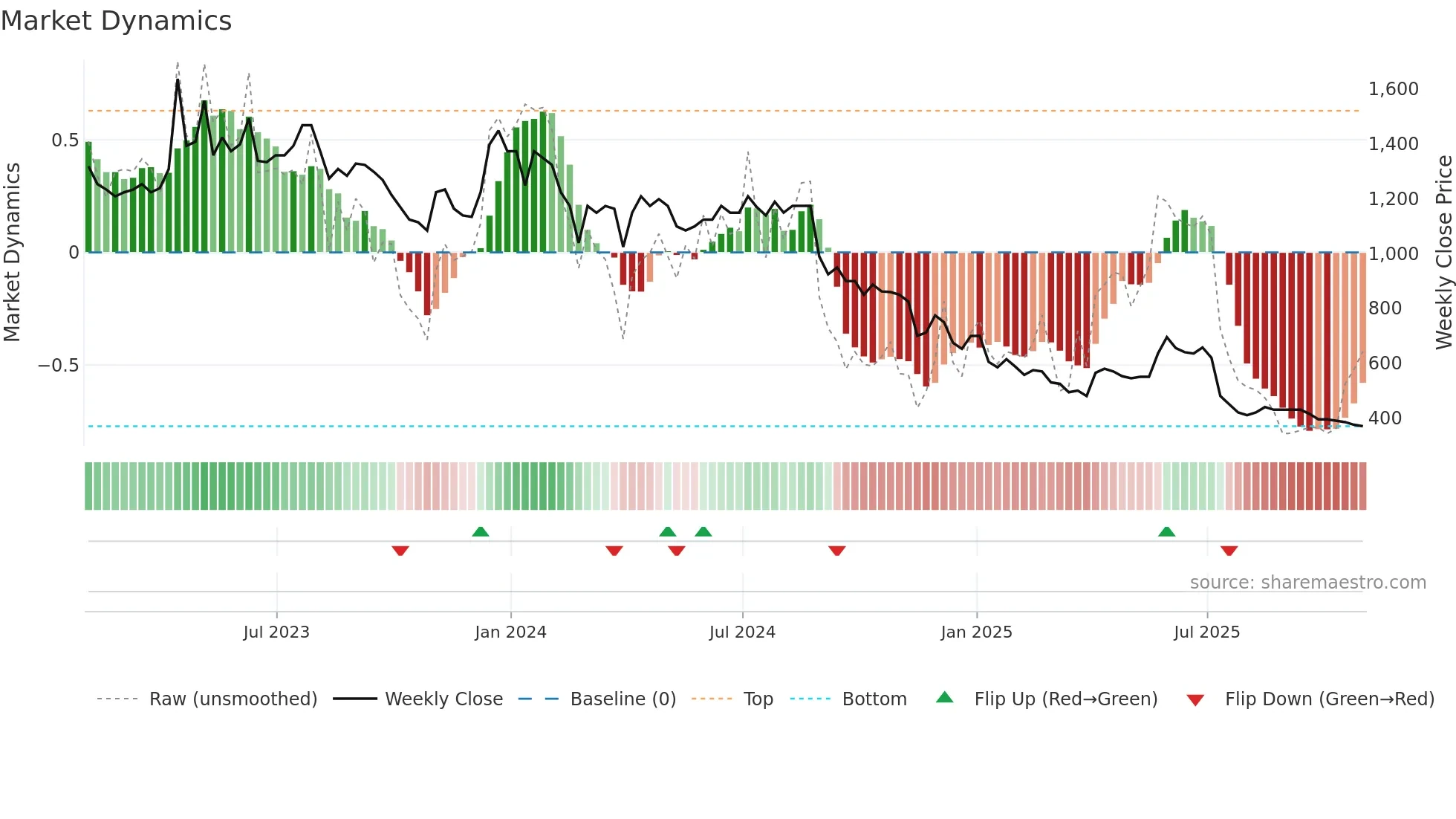

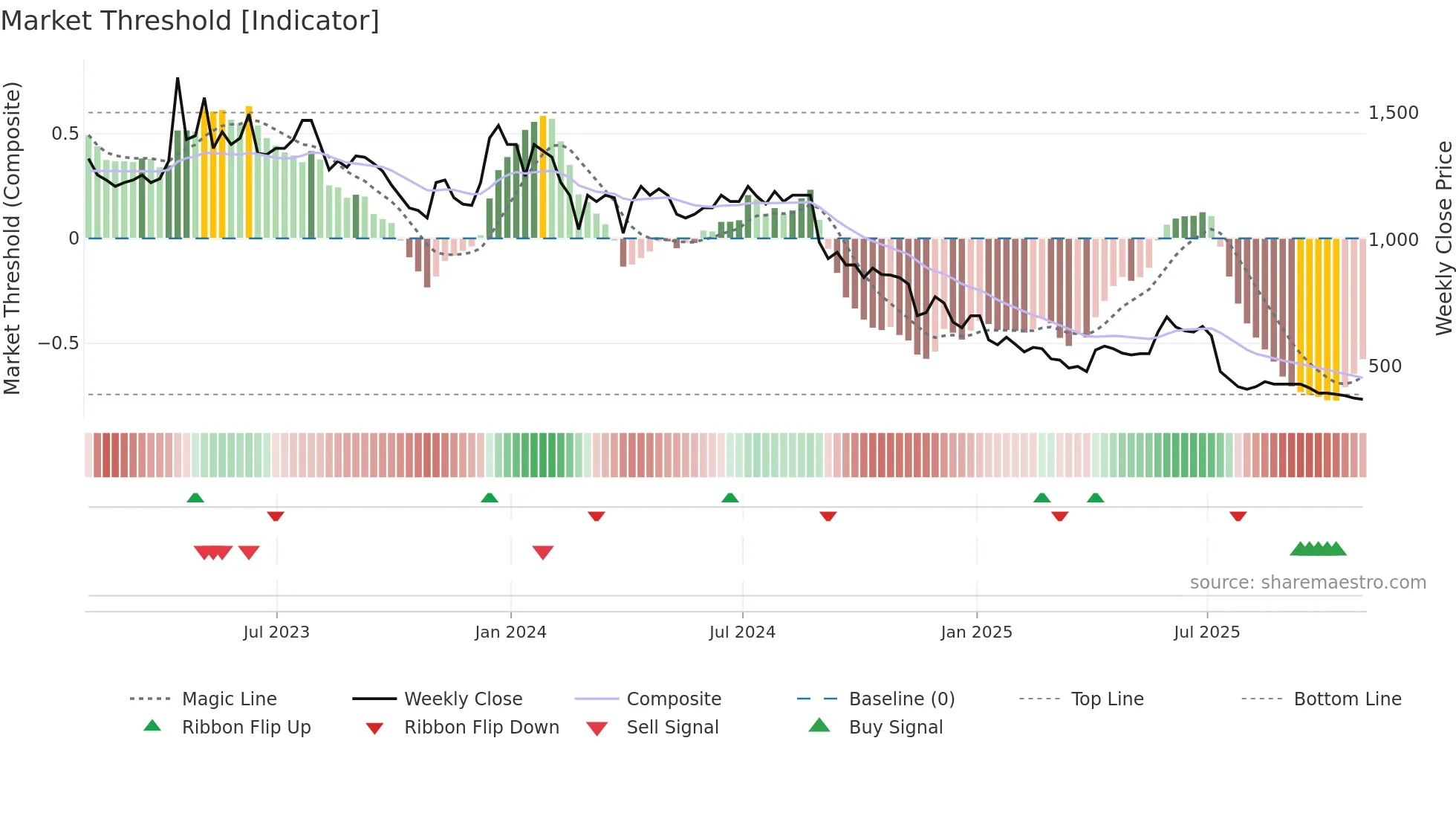

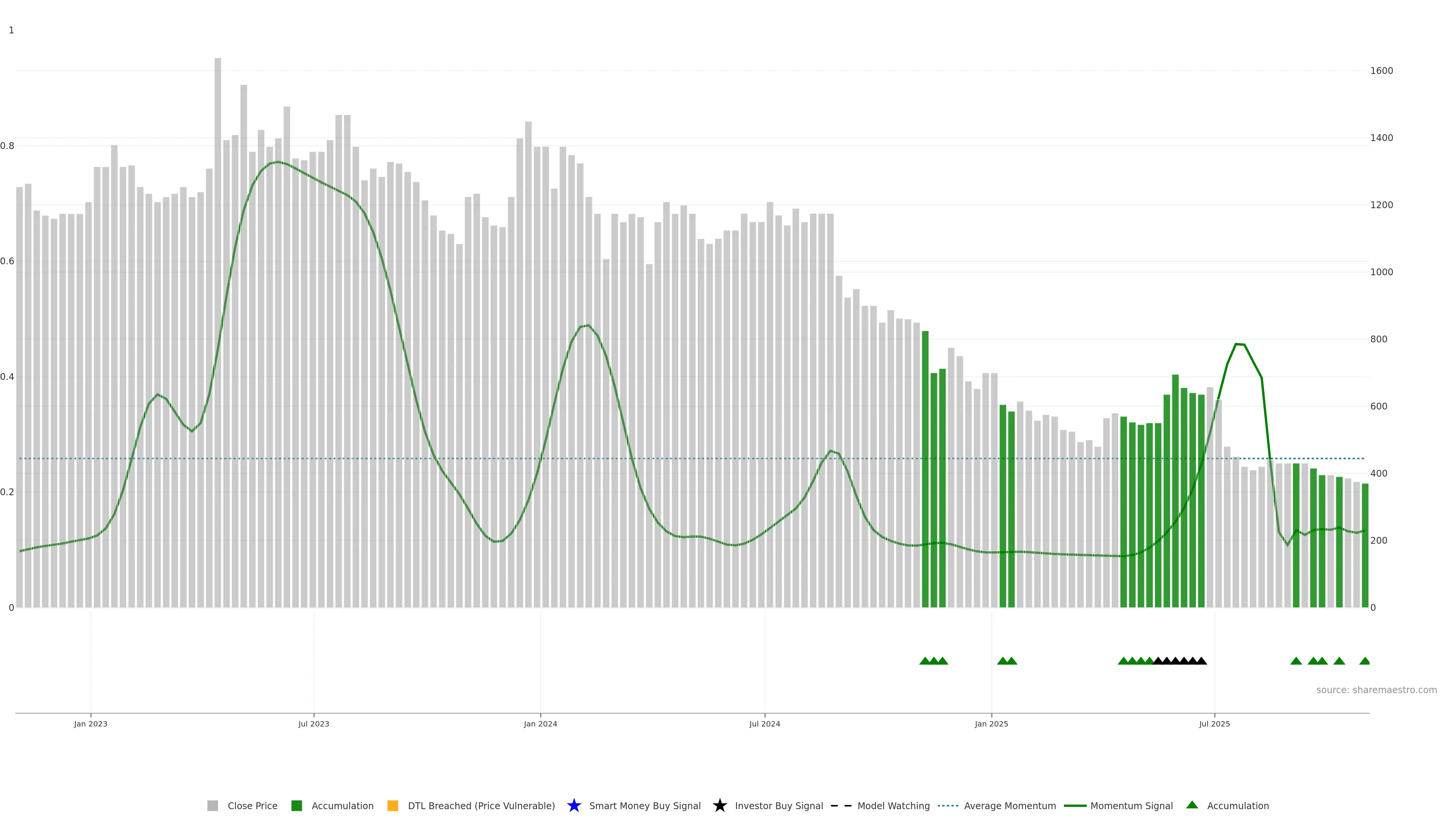

Smart Money

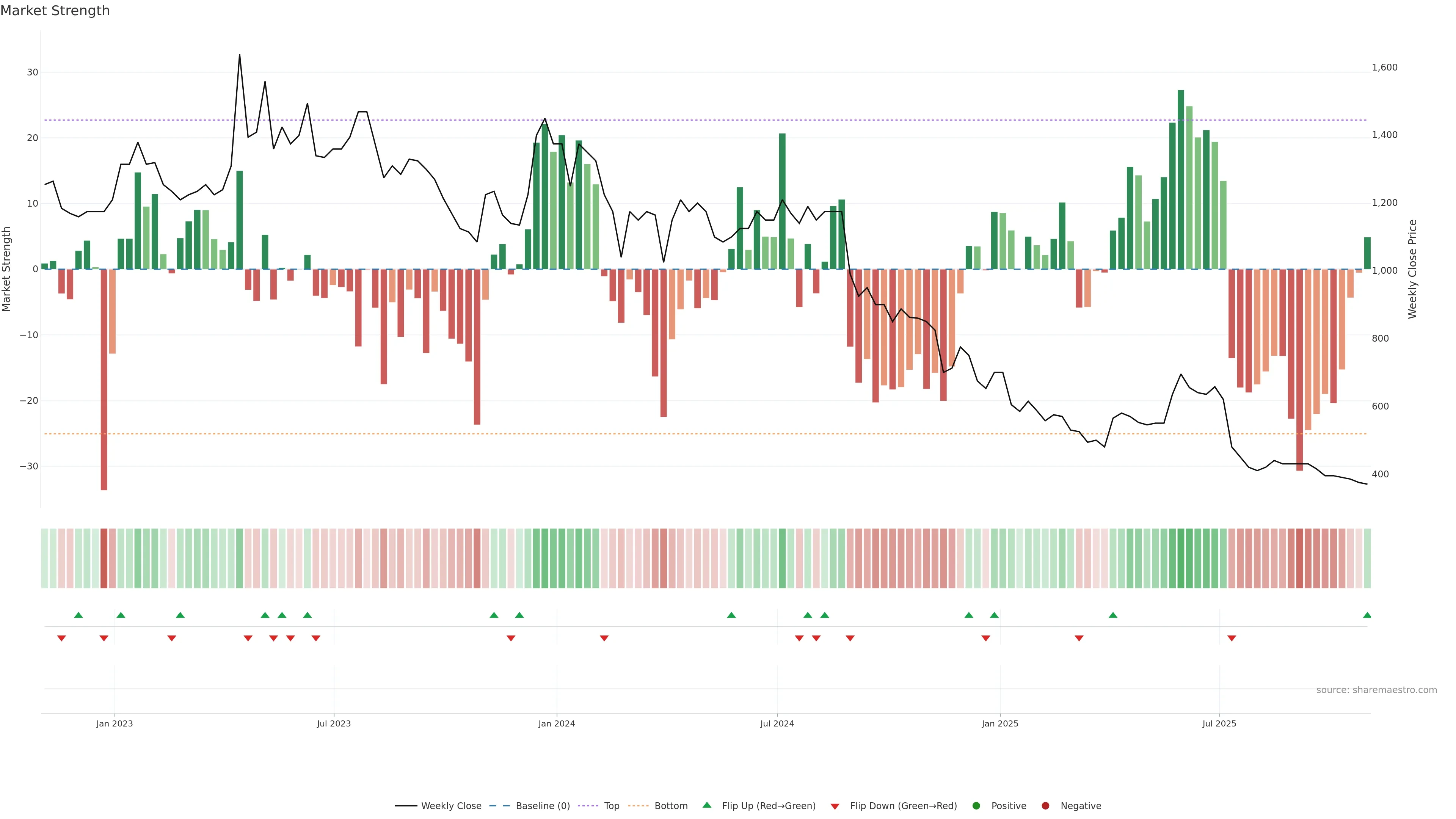

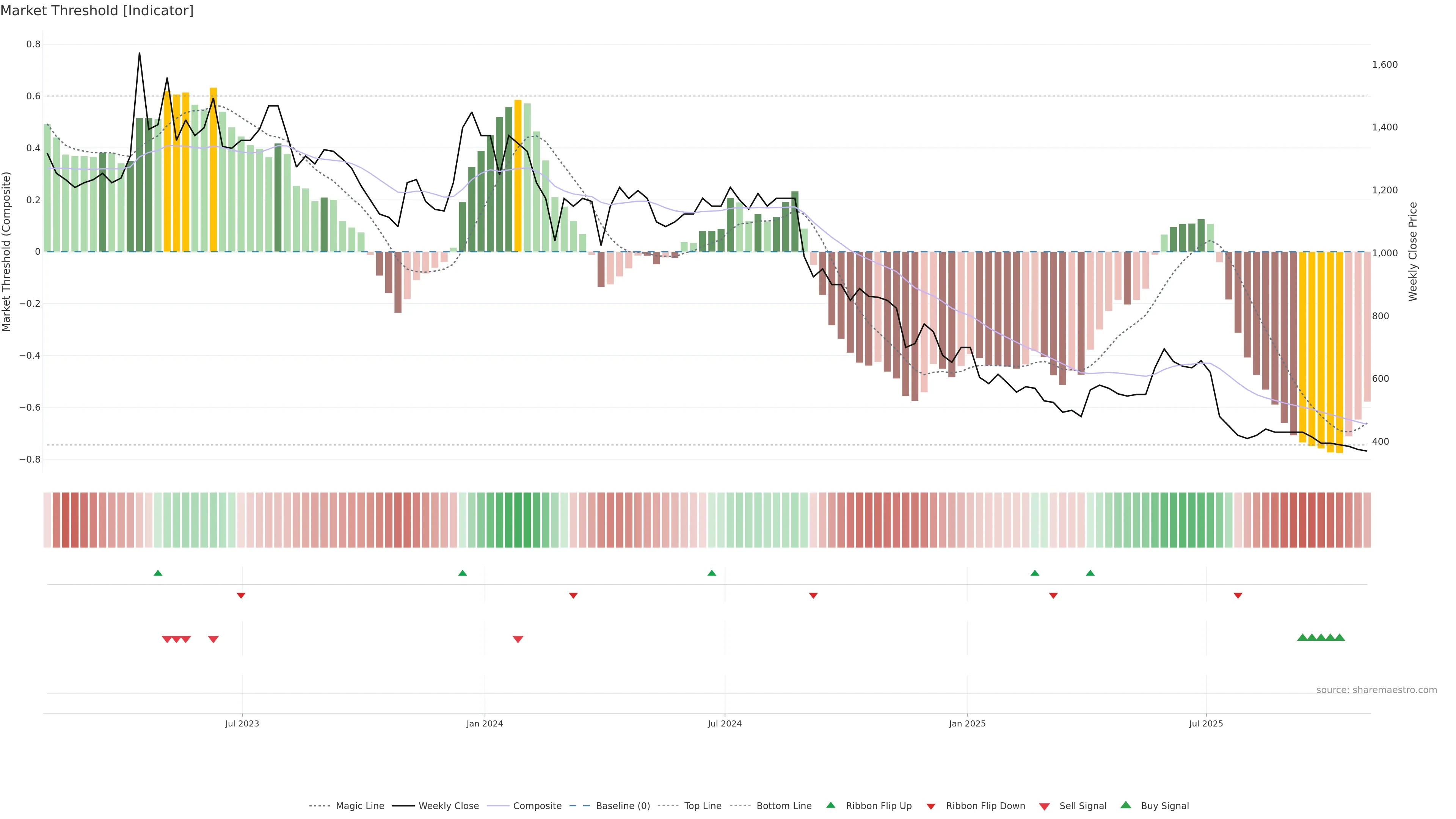

Early accumulation: trend rising from a depressed zone while pressure is sub-zero. — Often precedes Smart-Money style entries.

Score 0.75

+1 / -0

Early accumulation: trend rising from a depressed zone while pressure is sub-zero.

Early accumulation: trend rising from a depressed zone while pressure is sub-zero. Often precedes Smart-Money style entries. In essence this reflects institutional activity / accumulation-distribution patterns with a bullish tilt.

pol 0.75

conf 0.65

strong · high

What it means

Early accumulation: trend rising from a depressed zone while pressure is sub-zero. Often precedes Smart-Money style entries. In essence this reflects institutional activity / accumulation-distribution patterns with a bullish tilt.

Implications

Improves odds for follow-through if pullbacks hold higher lows. (pol 0.75, conf 0.65 → strong/high)

No additional observations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}