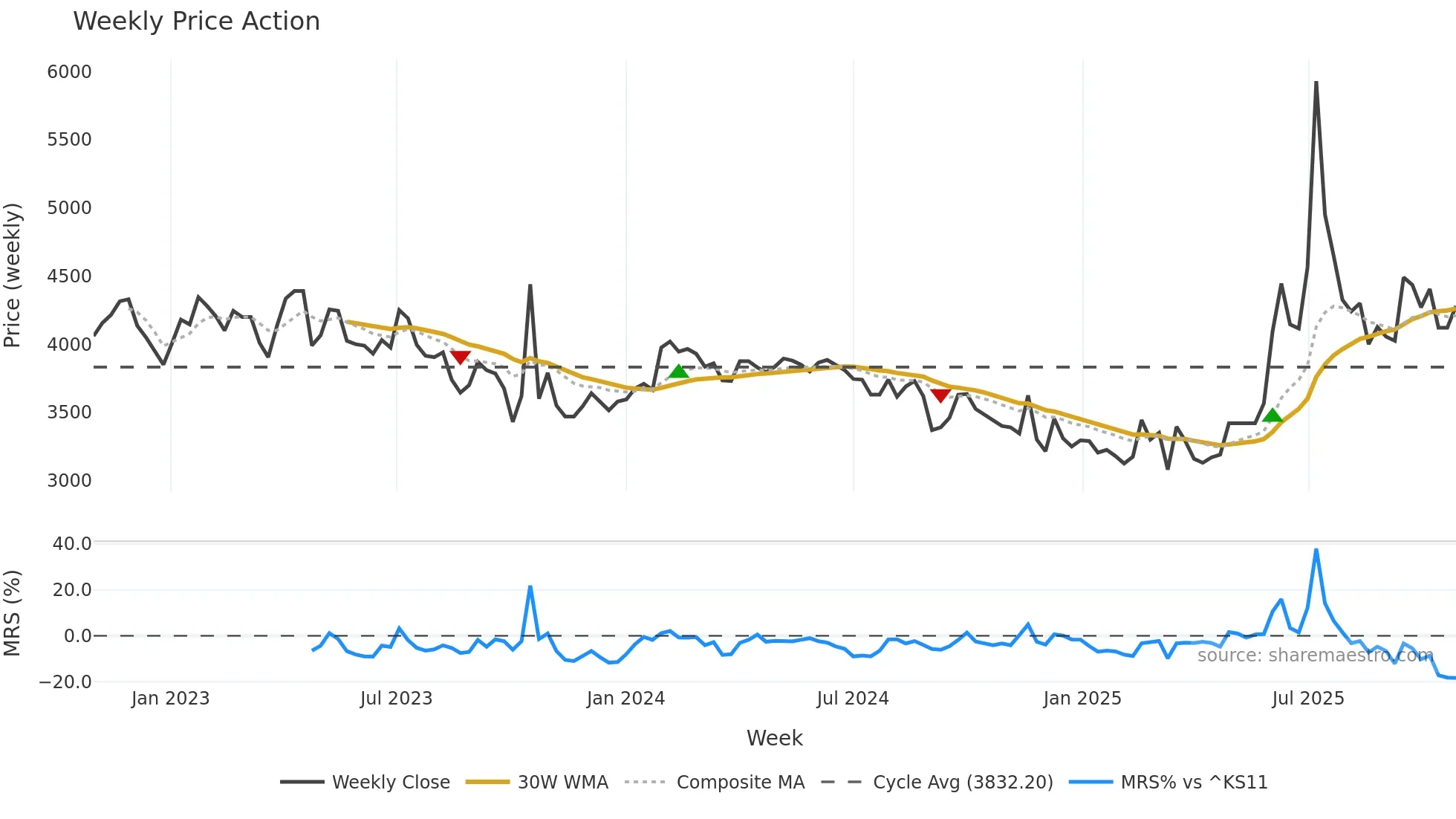

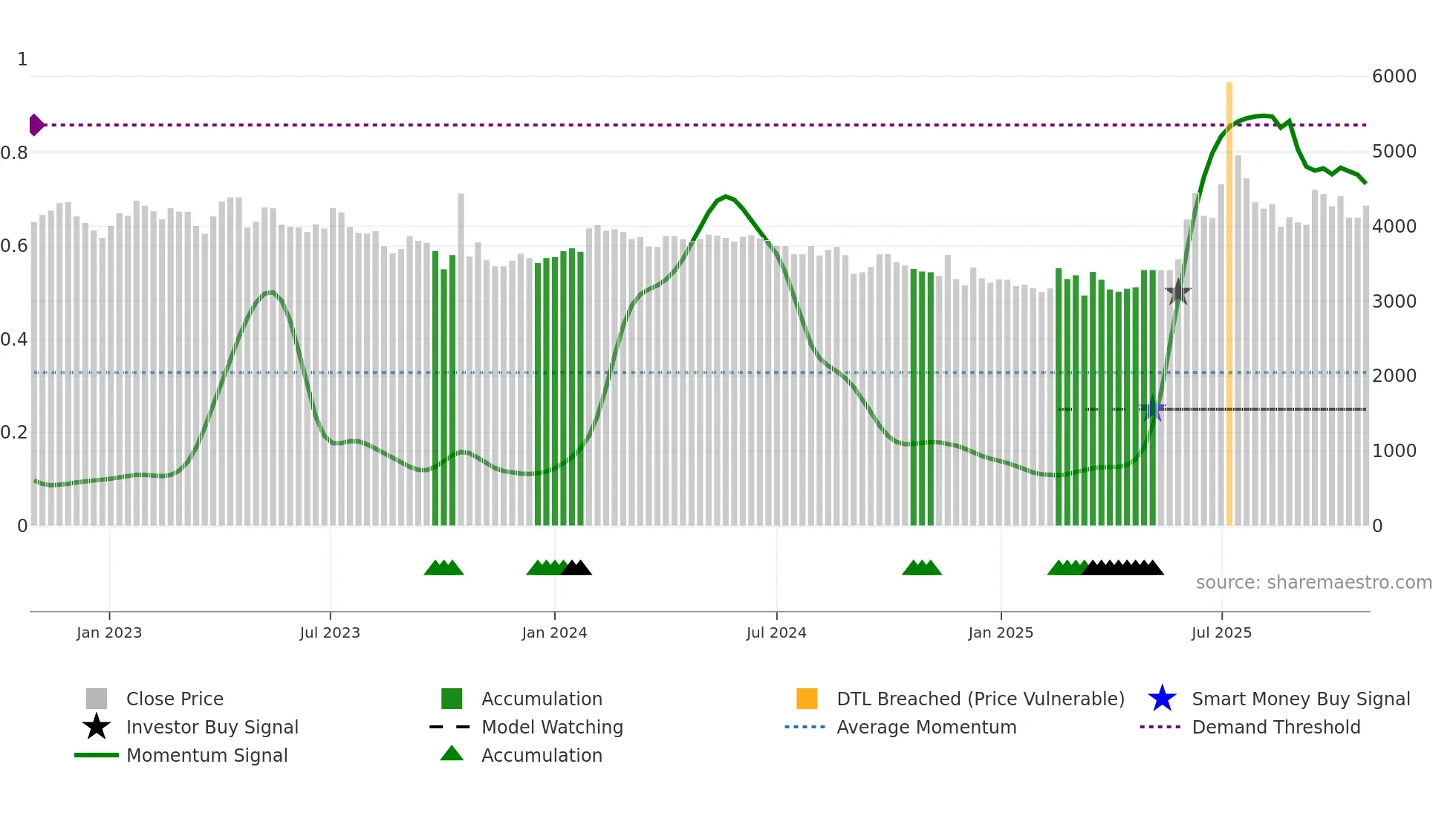

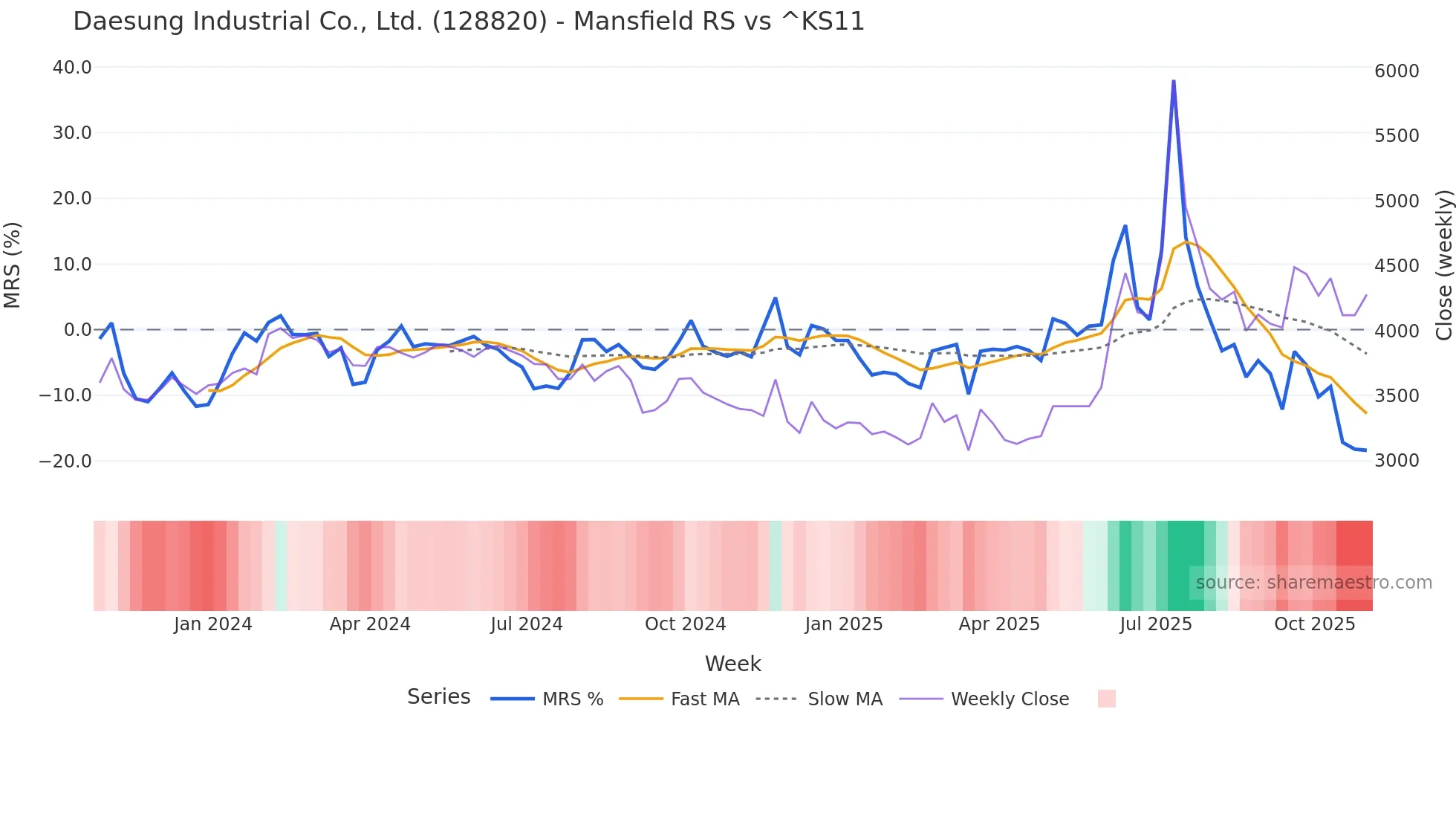

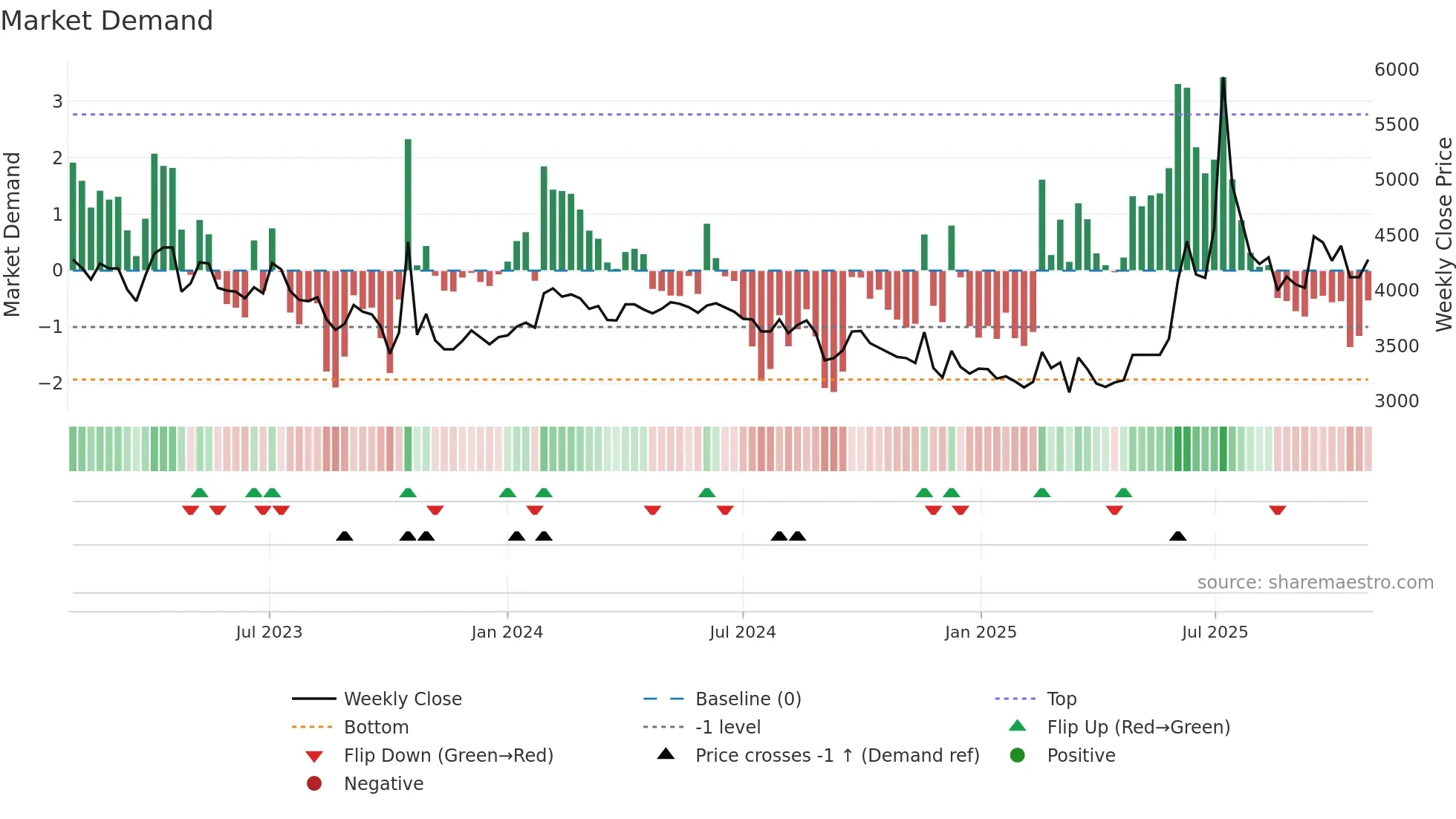

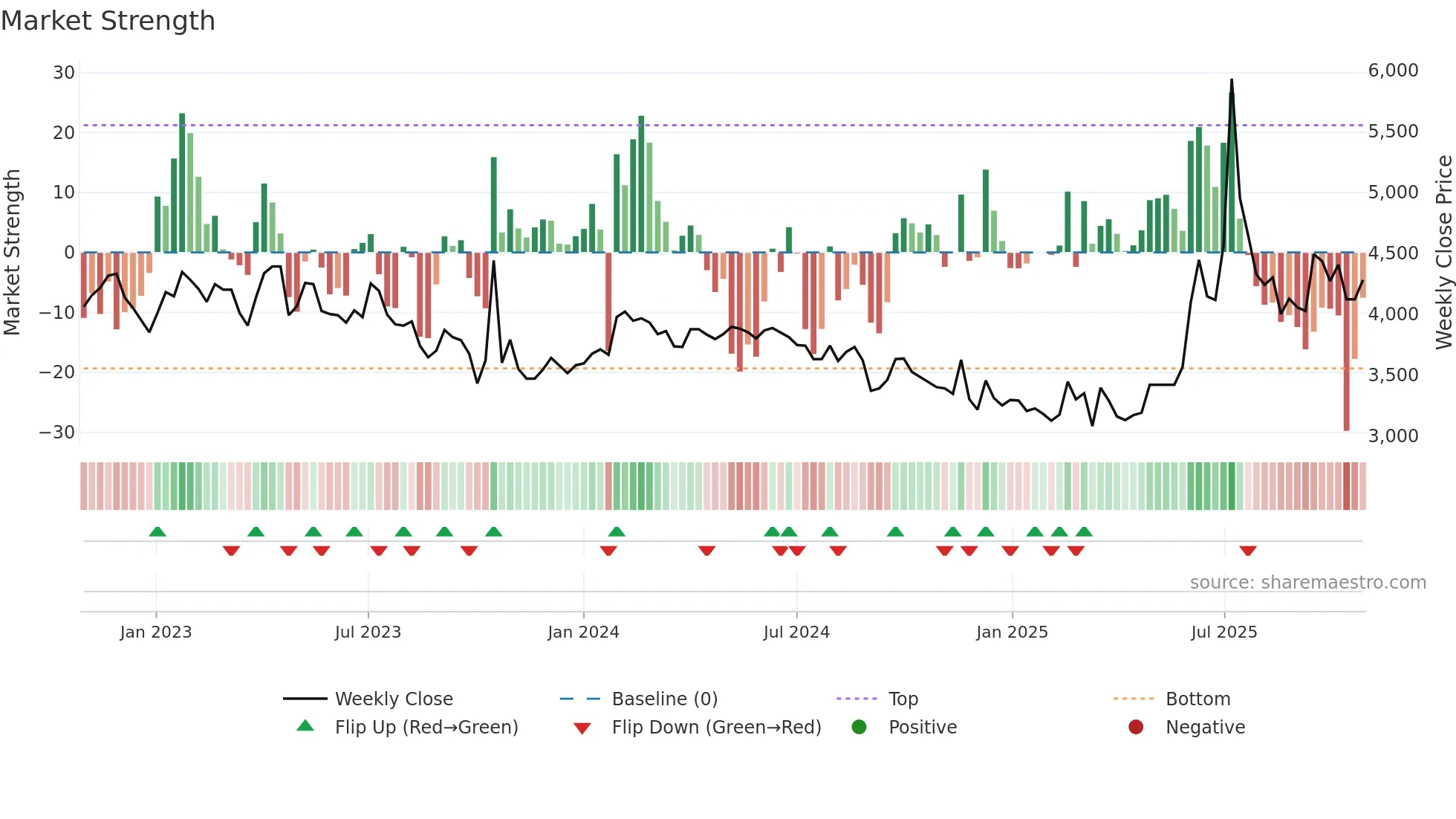

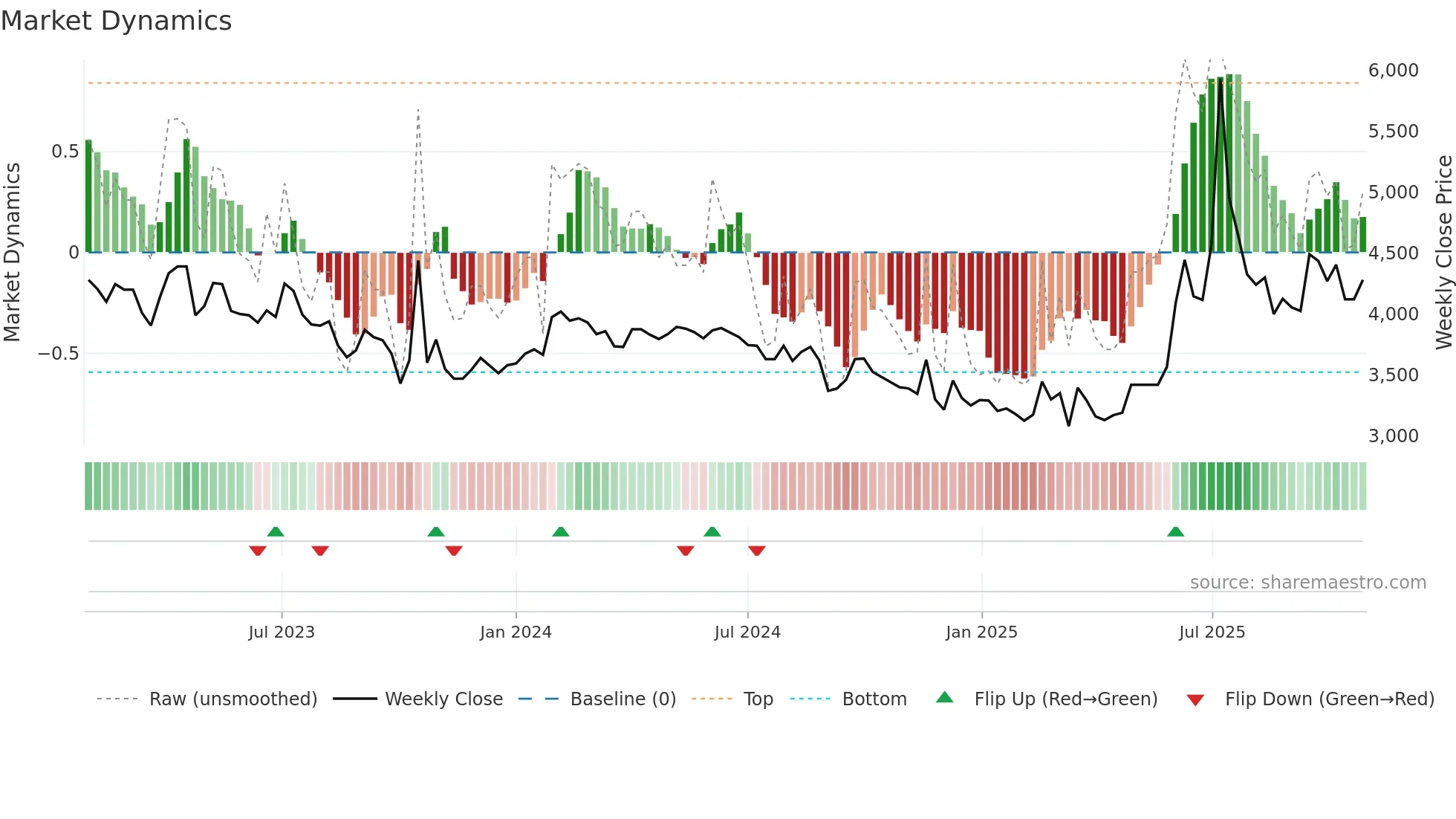

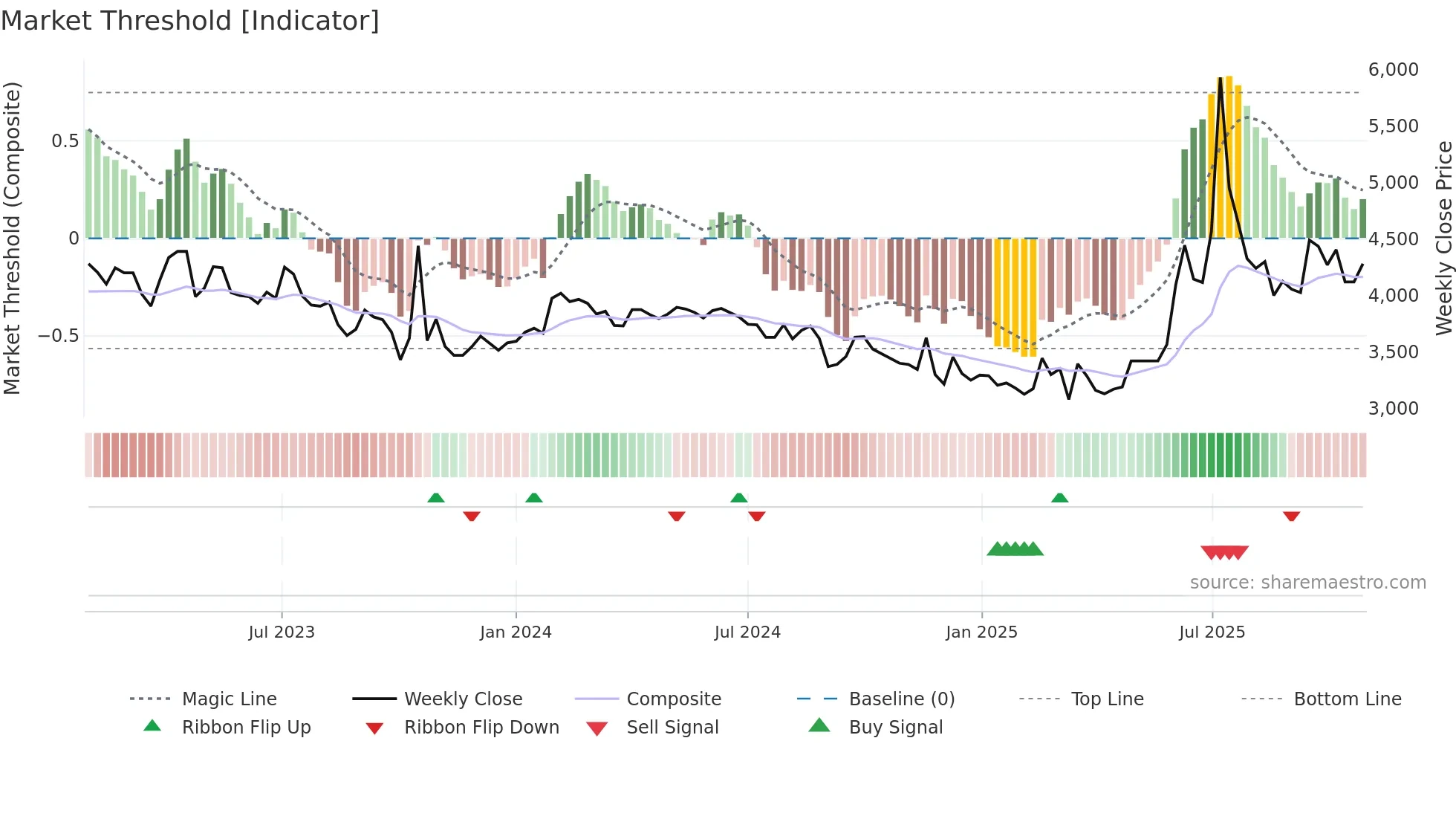

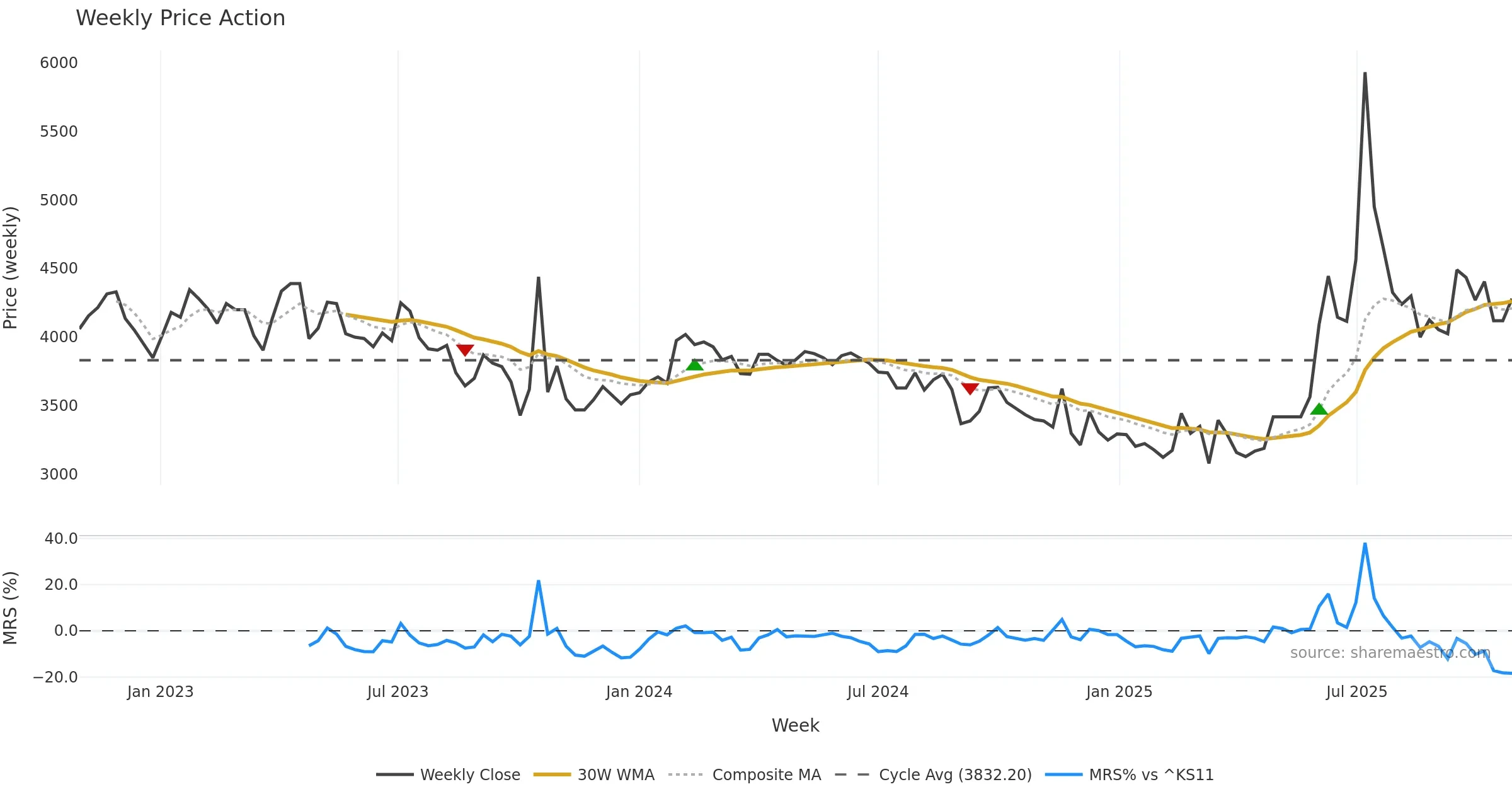

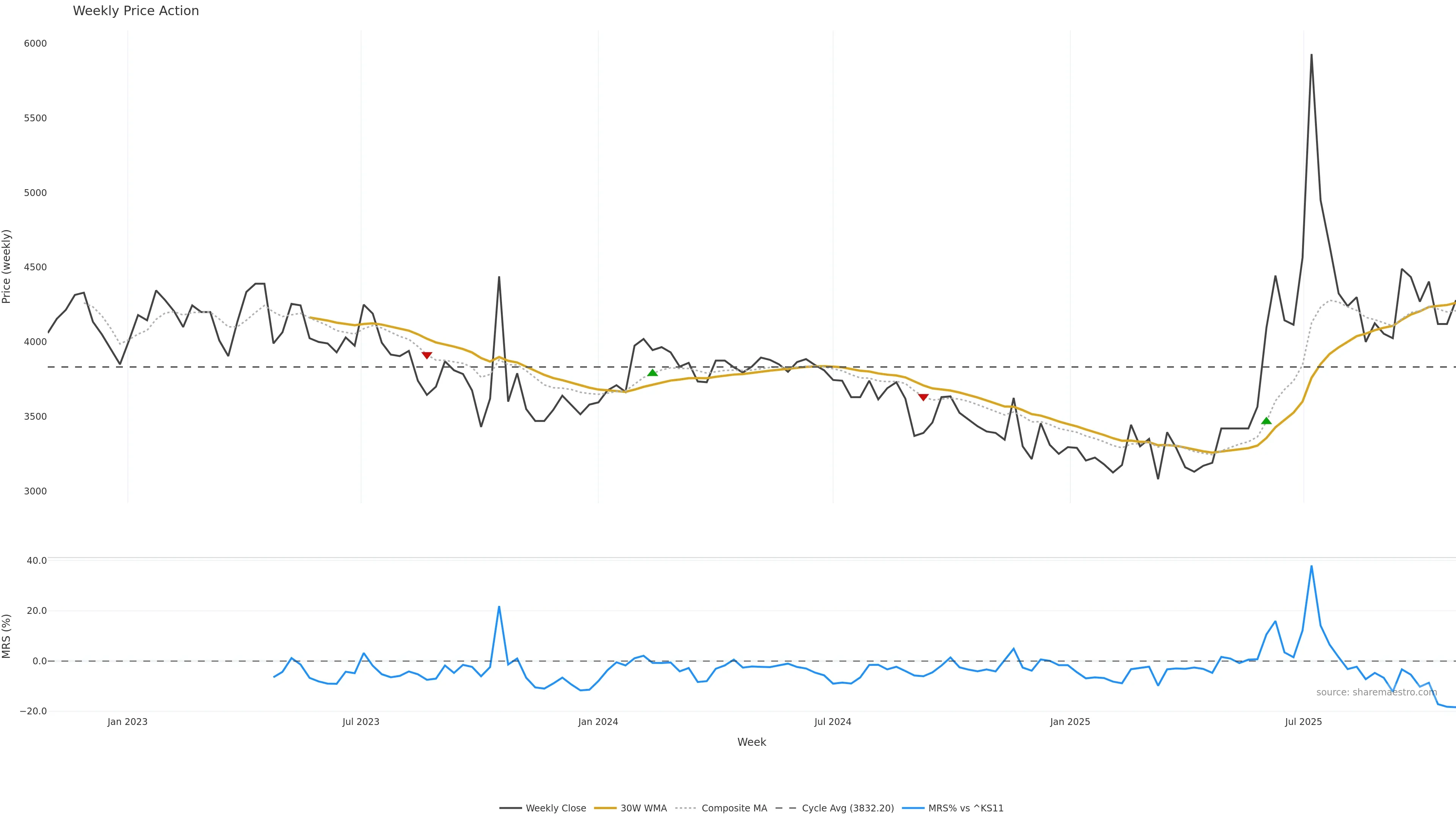

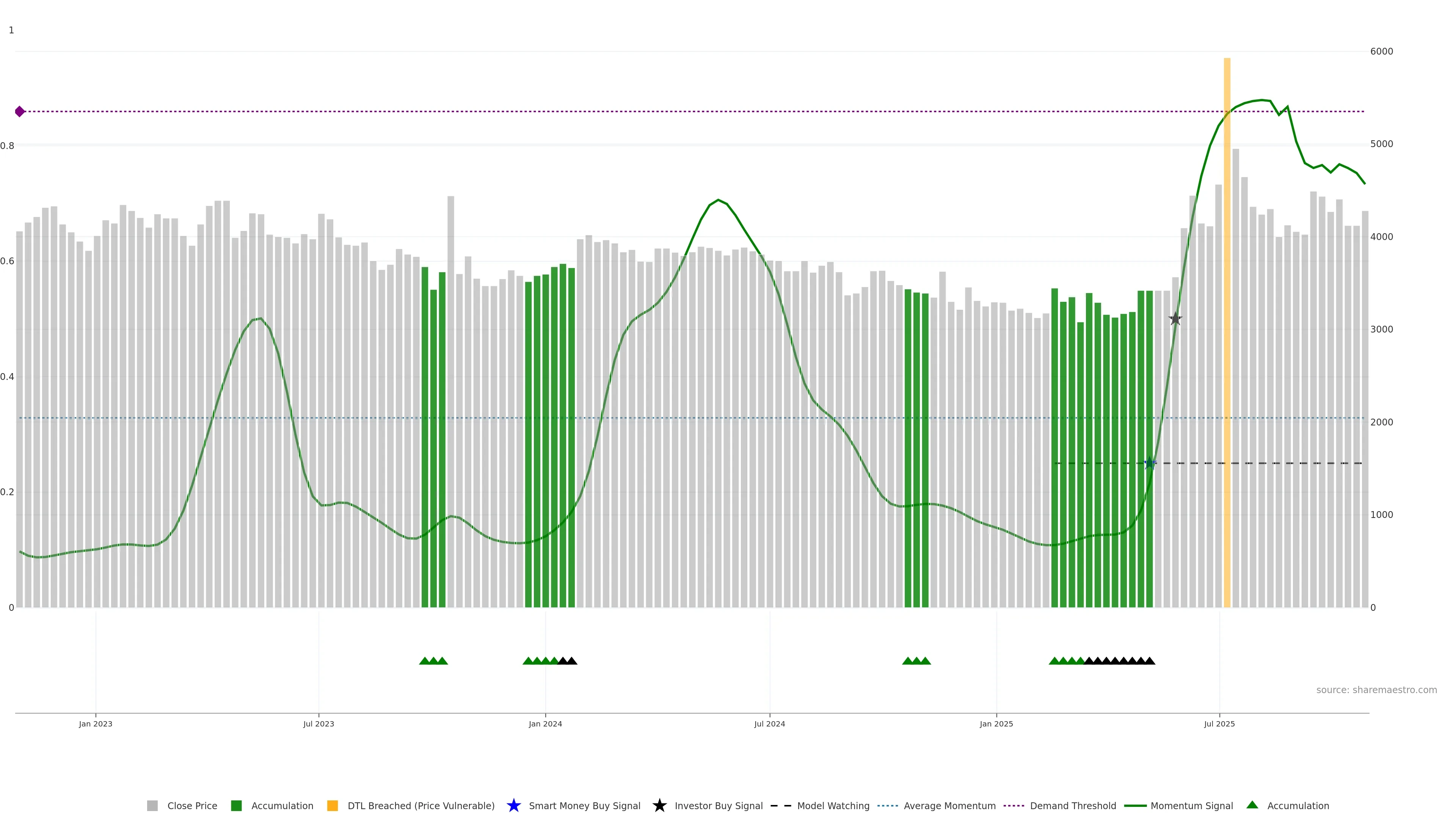

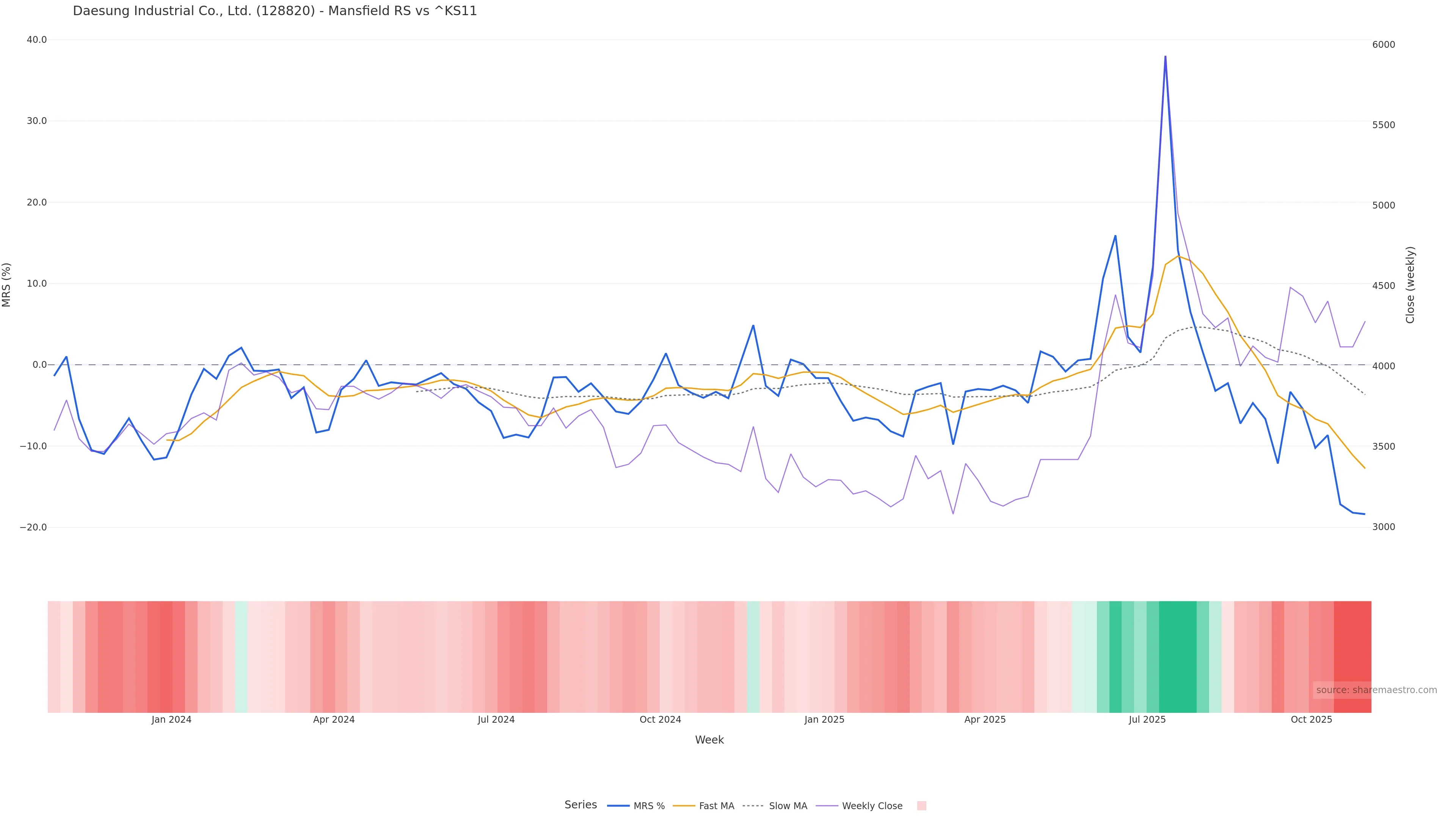

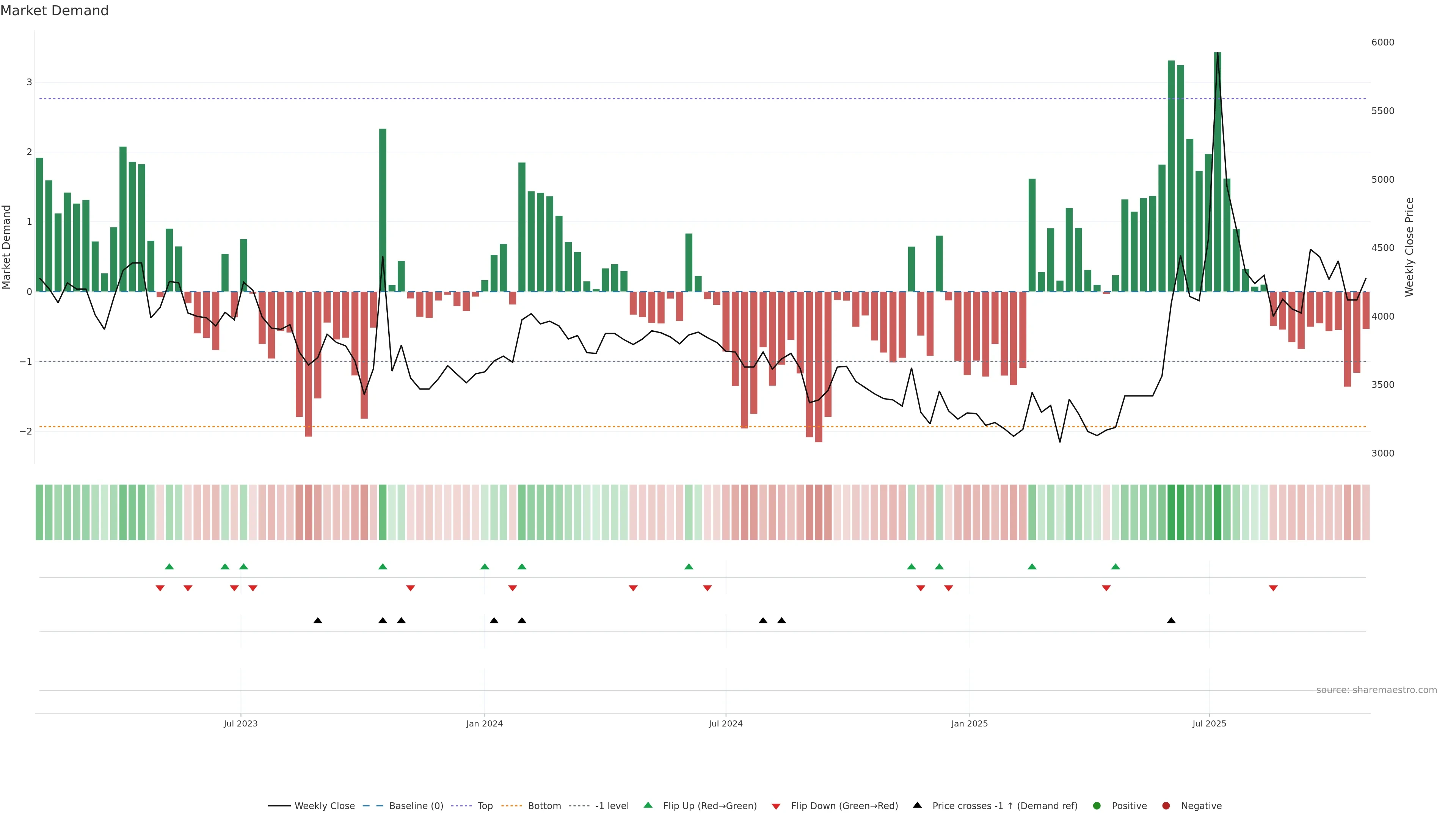

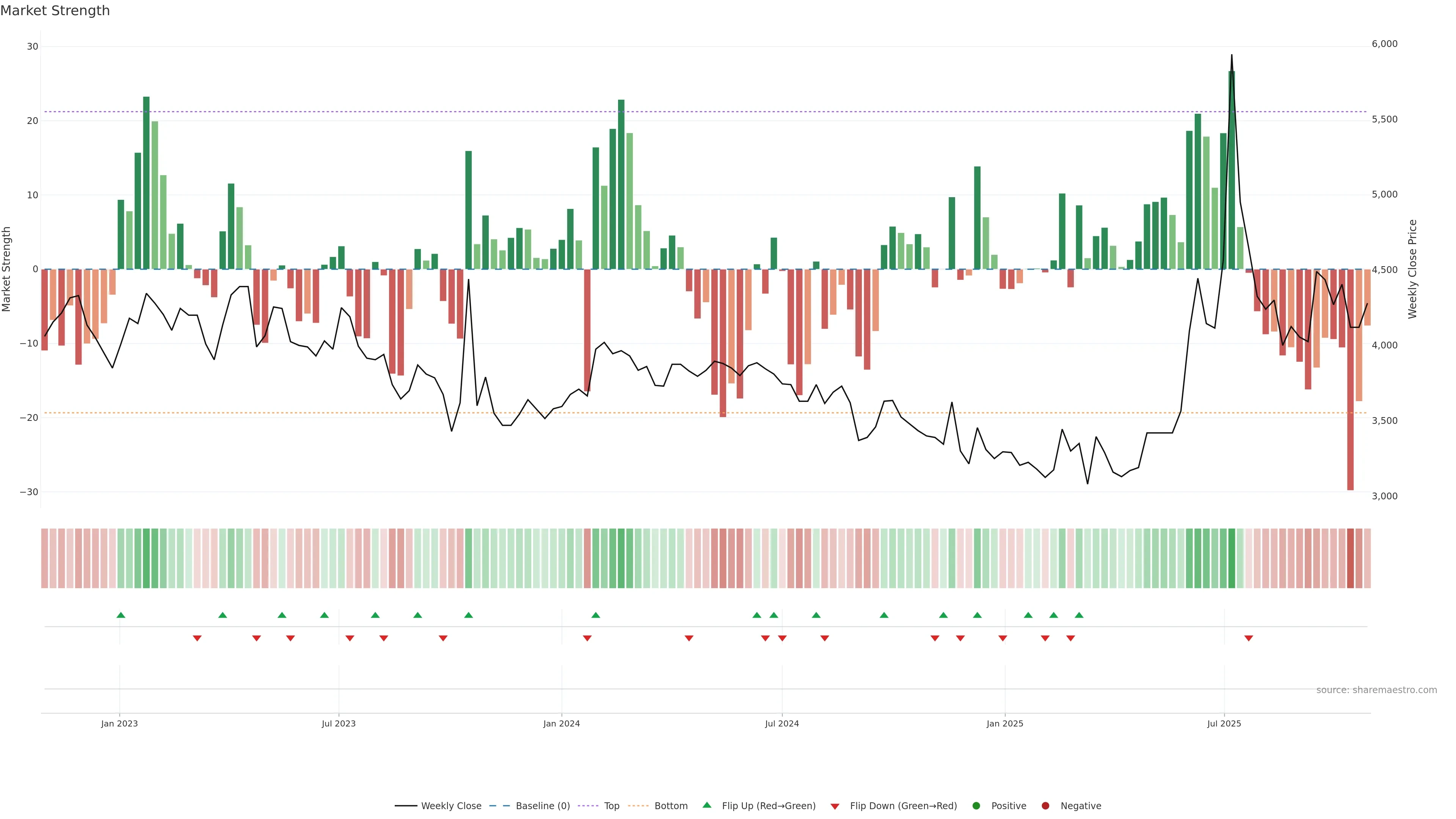

Market Strength

Relative Strength is negative and deteriorating. — Avoid laggards unless a reversal pattern forms.

Score -0.55

+0 / -1

Level -7.614

Relative Strength is negative and deteriorating.

Relative Strength is negative and deteriorating. Avoid laggards unless a reversal pattern forms. In essence this reflects relative strength vs peers/benchmarks with a bearish tilt.

pol -0.55

conf 0.6

moderate · medium

What it means

Relative Strength is negative and deteriorating. Avoid laggards unless a reversal pattern forms. In essence this reflects relative strength vs peers/benchmarks with a bearish tilt.

Implications

Raises risk of failed breakouts; strength must prove itself on closes. (pol -0.55, conf 0.60 → moderate/medium)

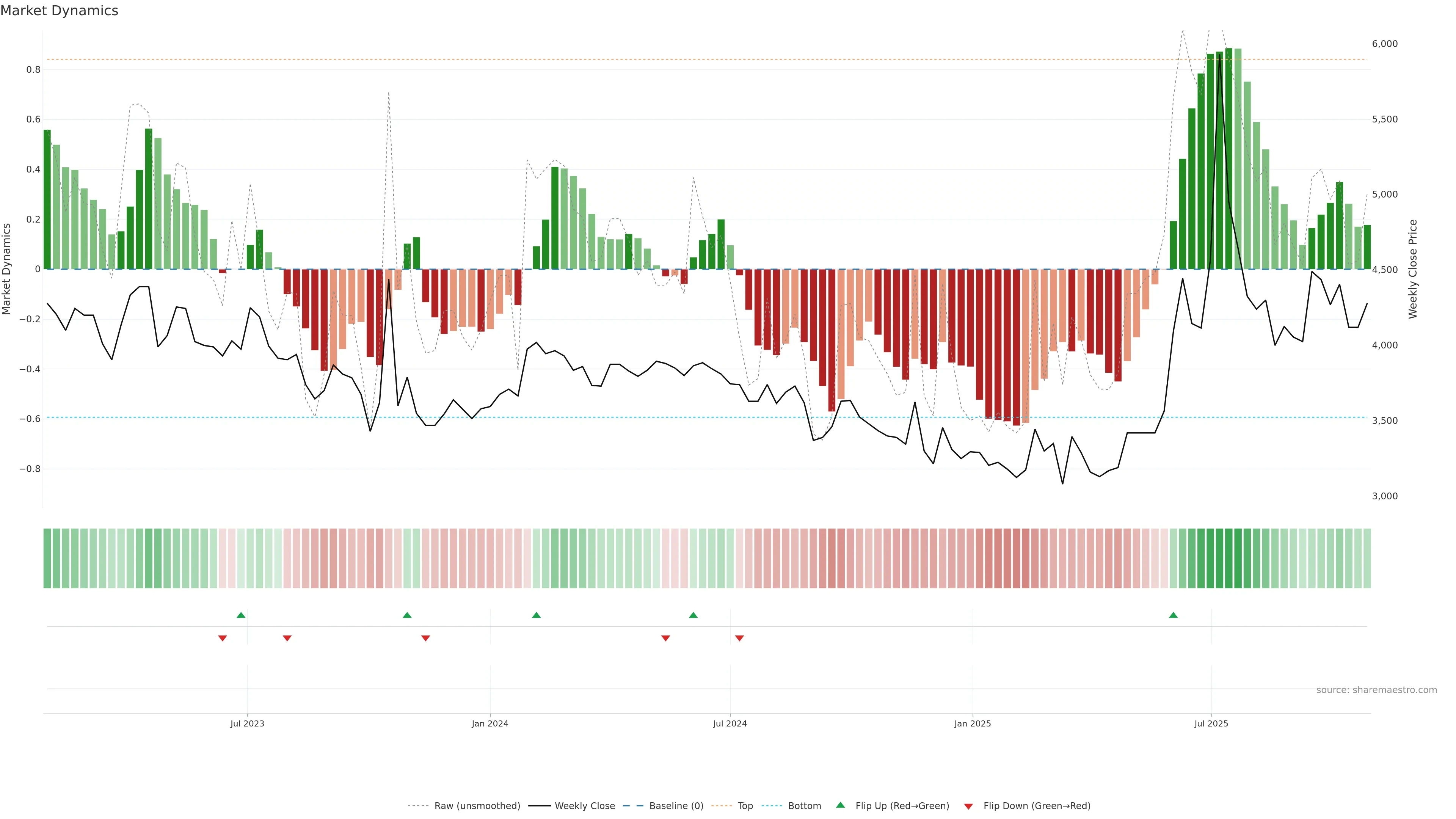

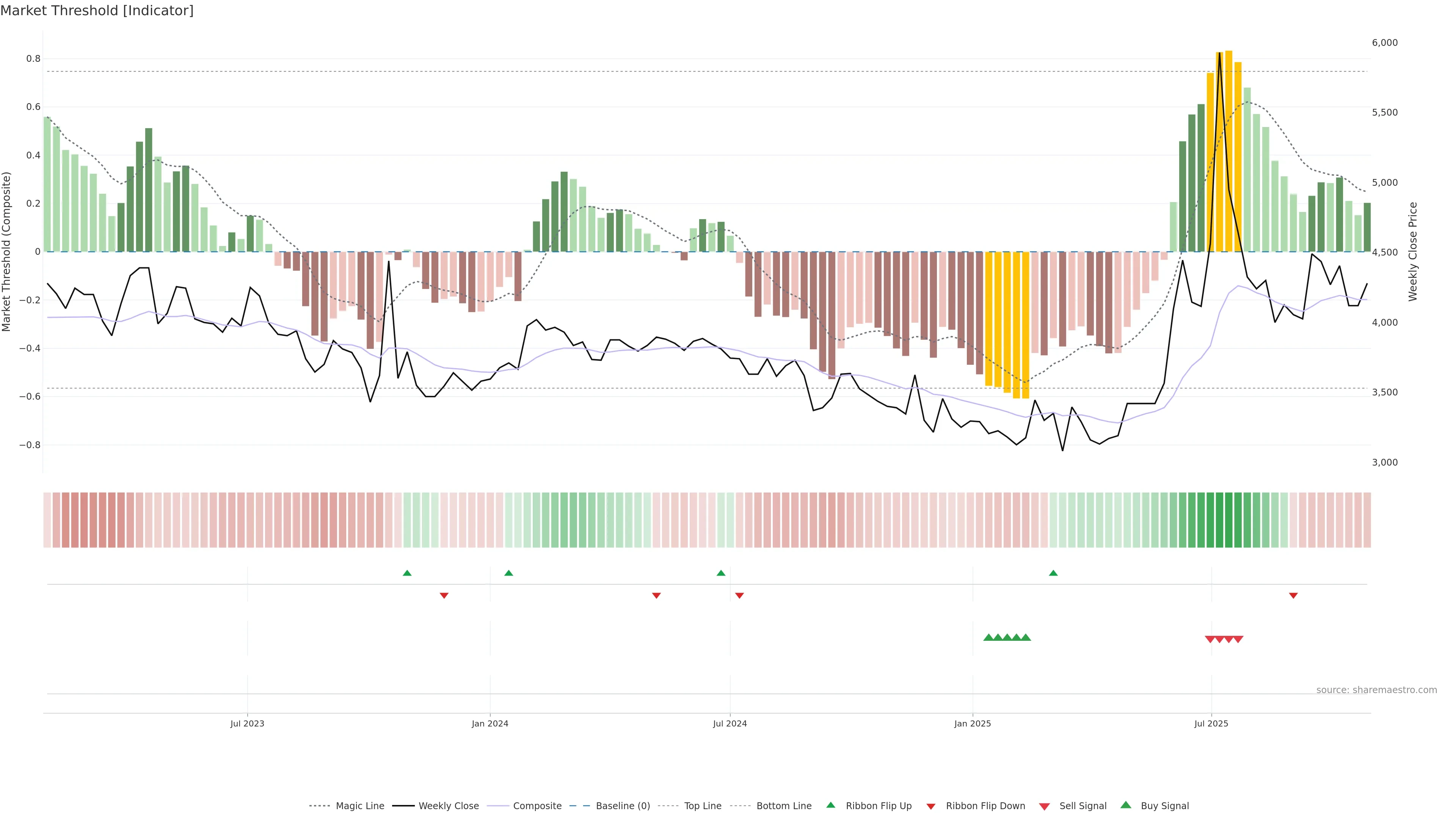

No additional observations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}