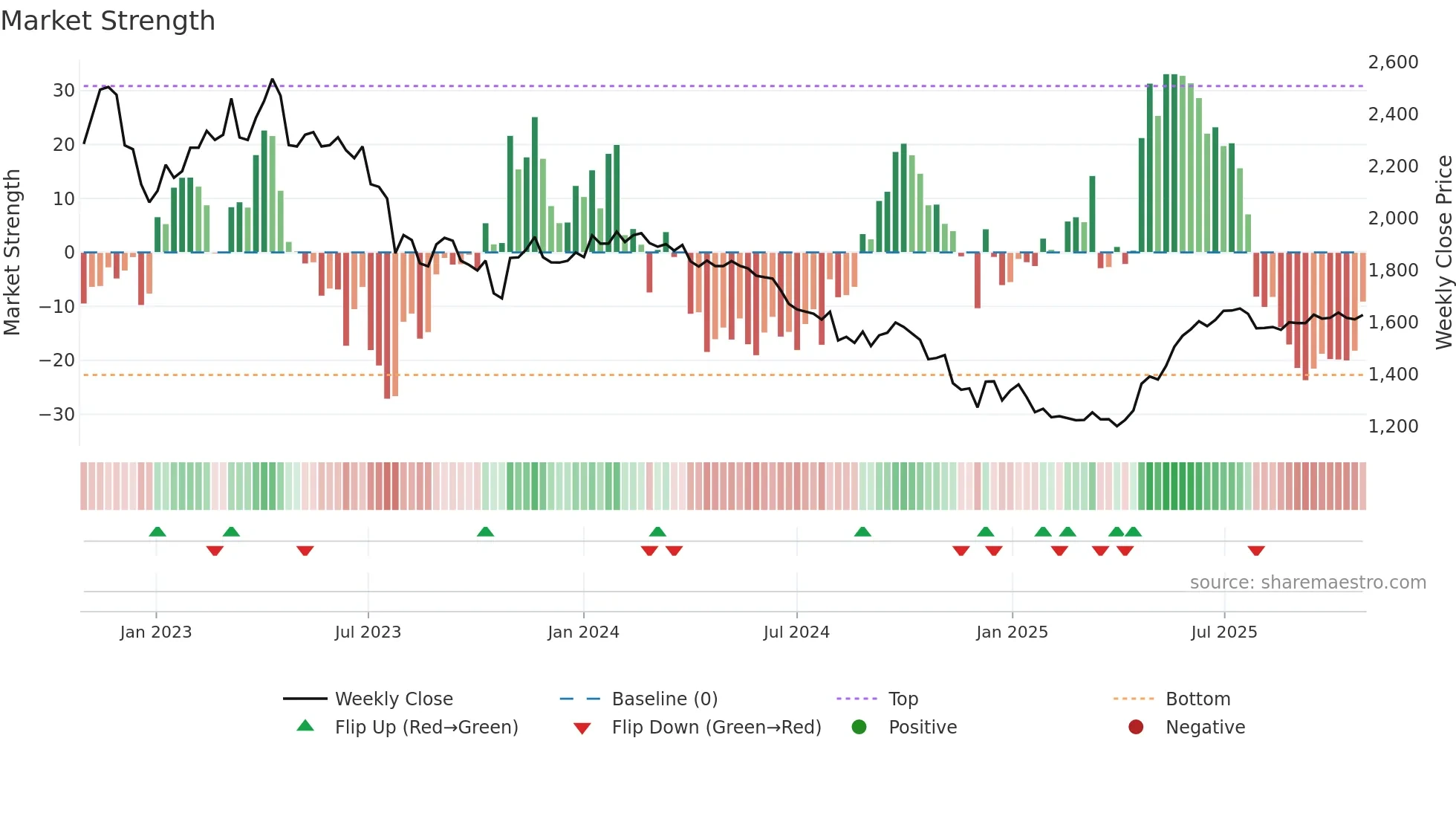

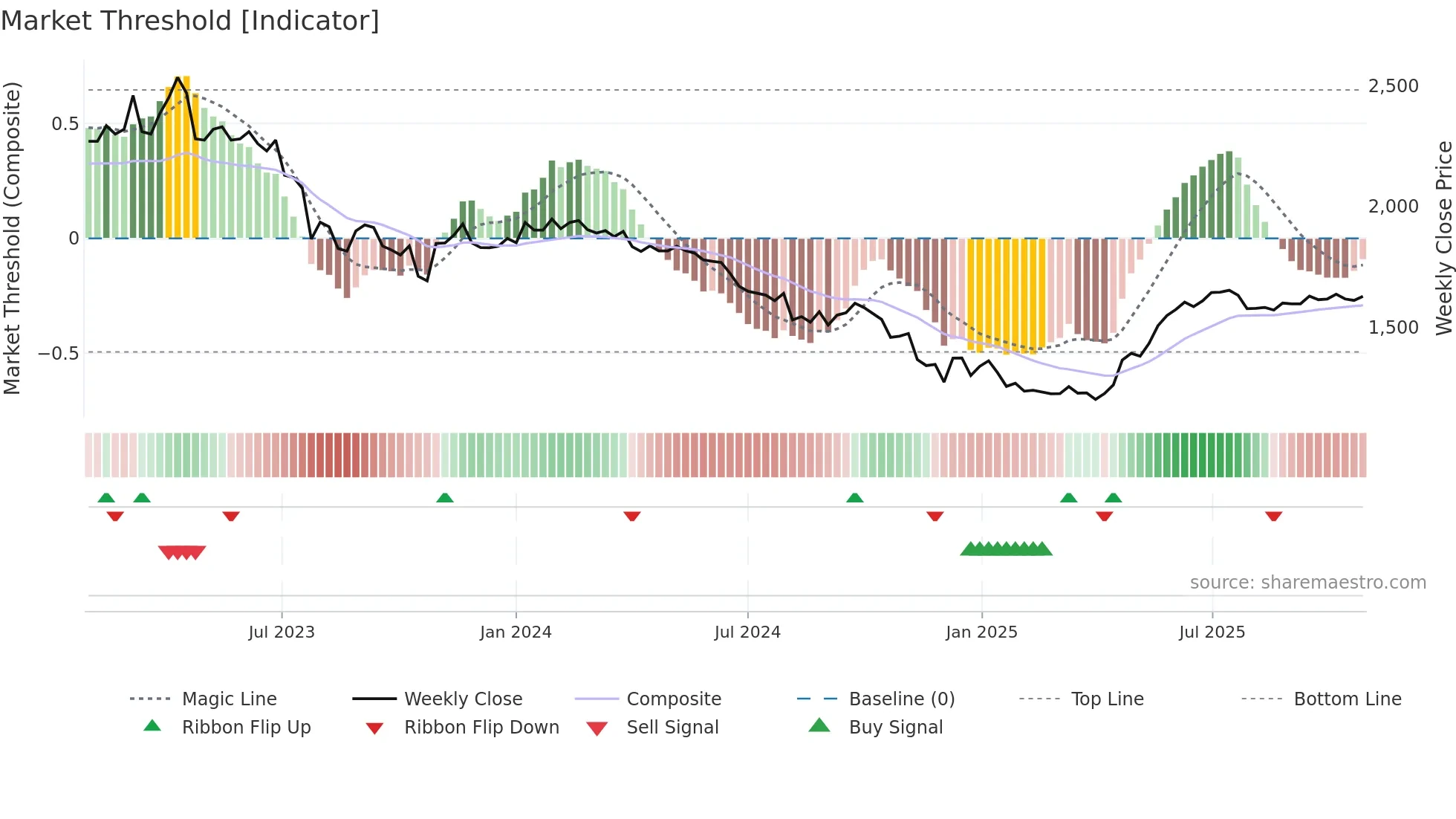

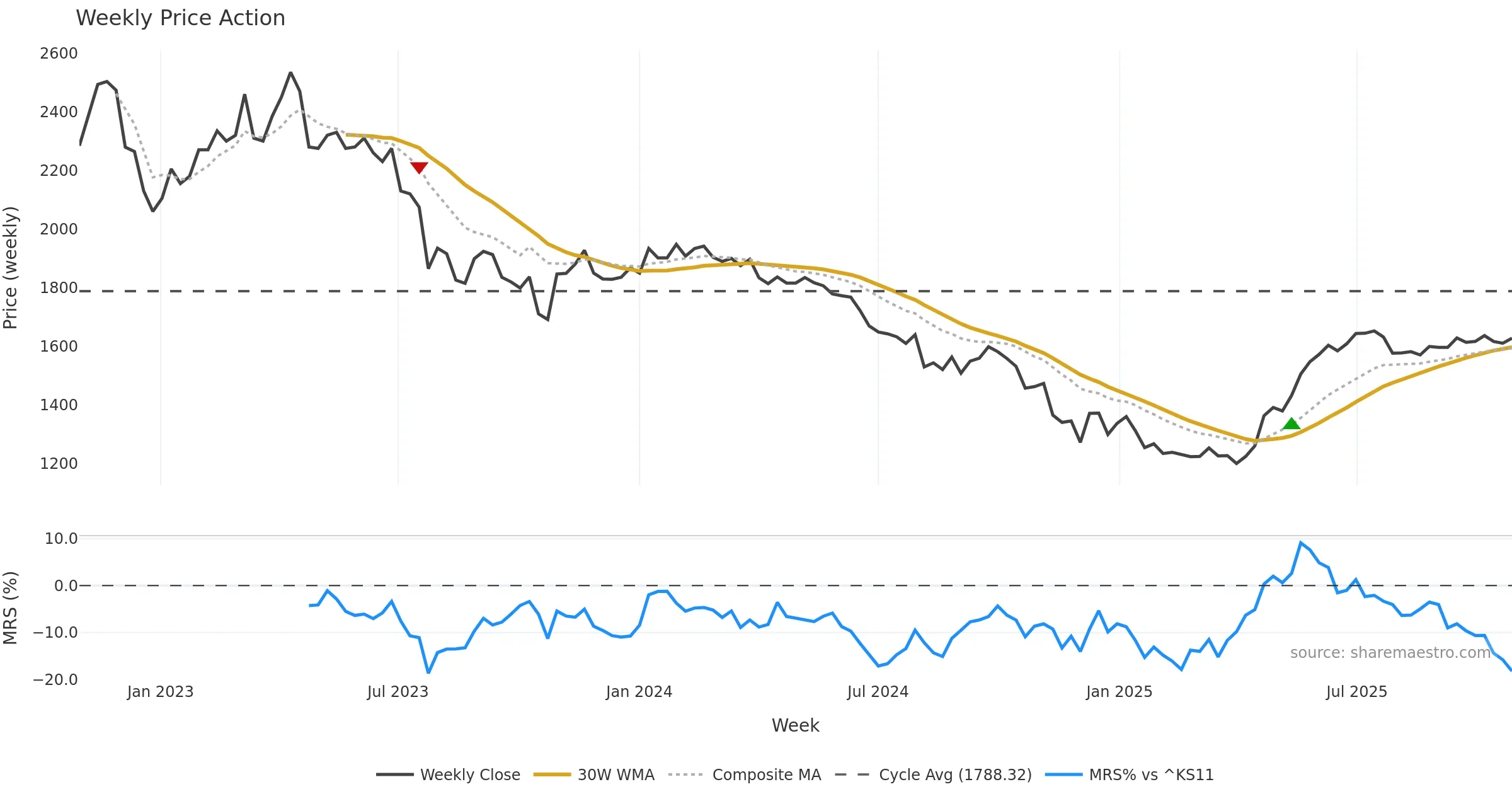

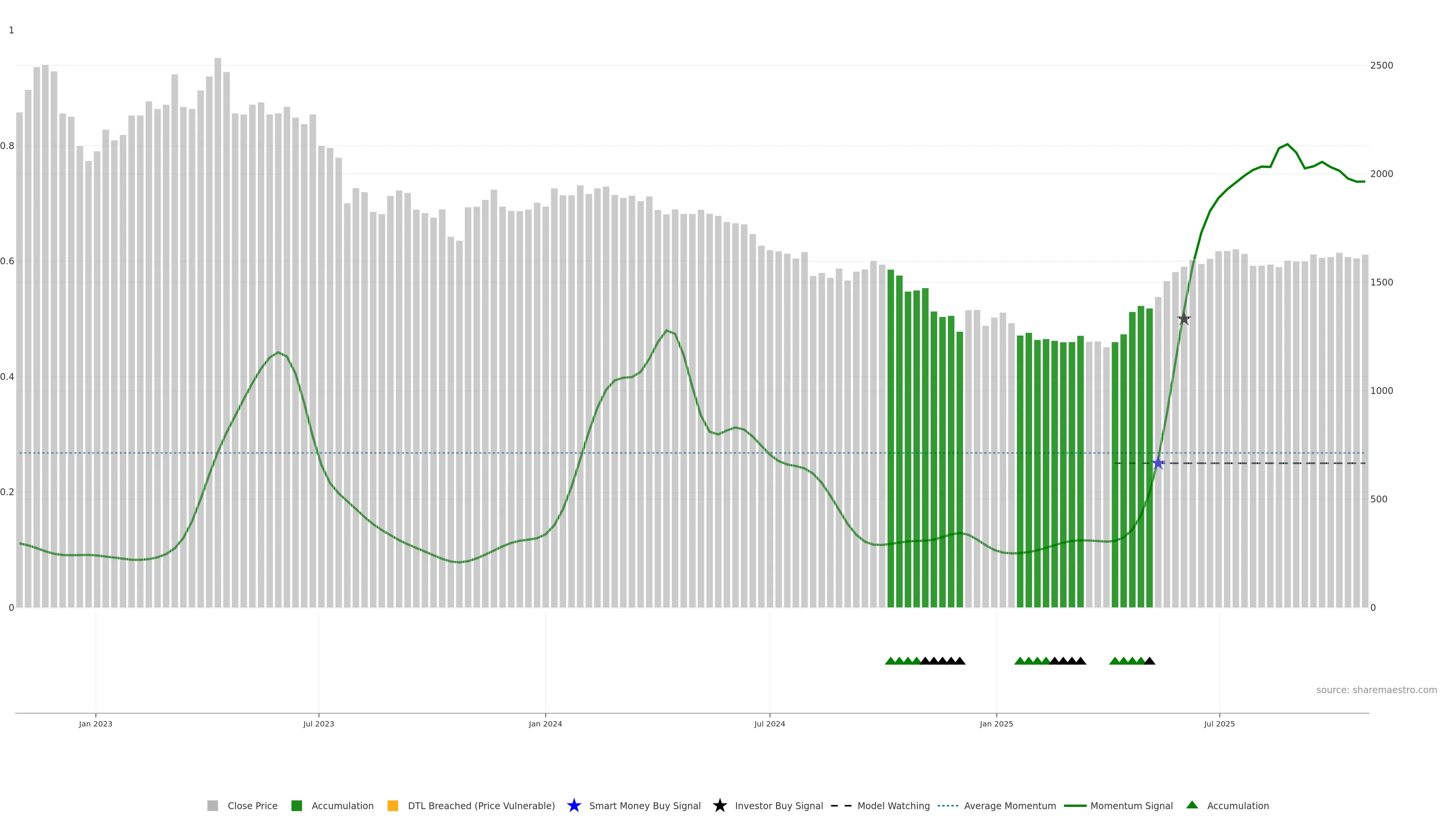

Market Dynamics

Dynamics turning up from negative territory. — Early trend repair often precedes price strength.

Score 0.7

+2 / -0

Level -0.105

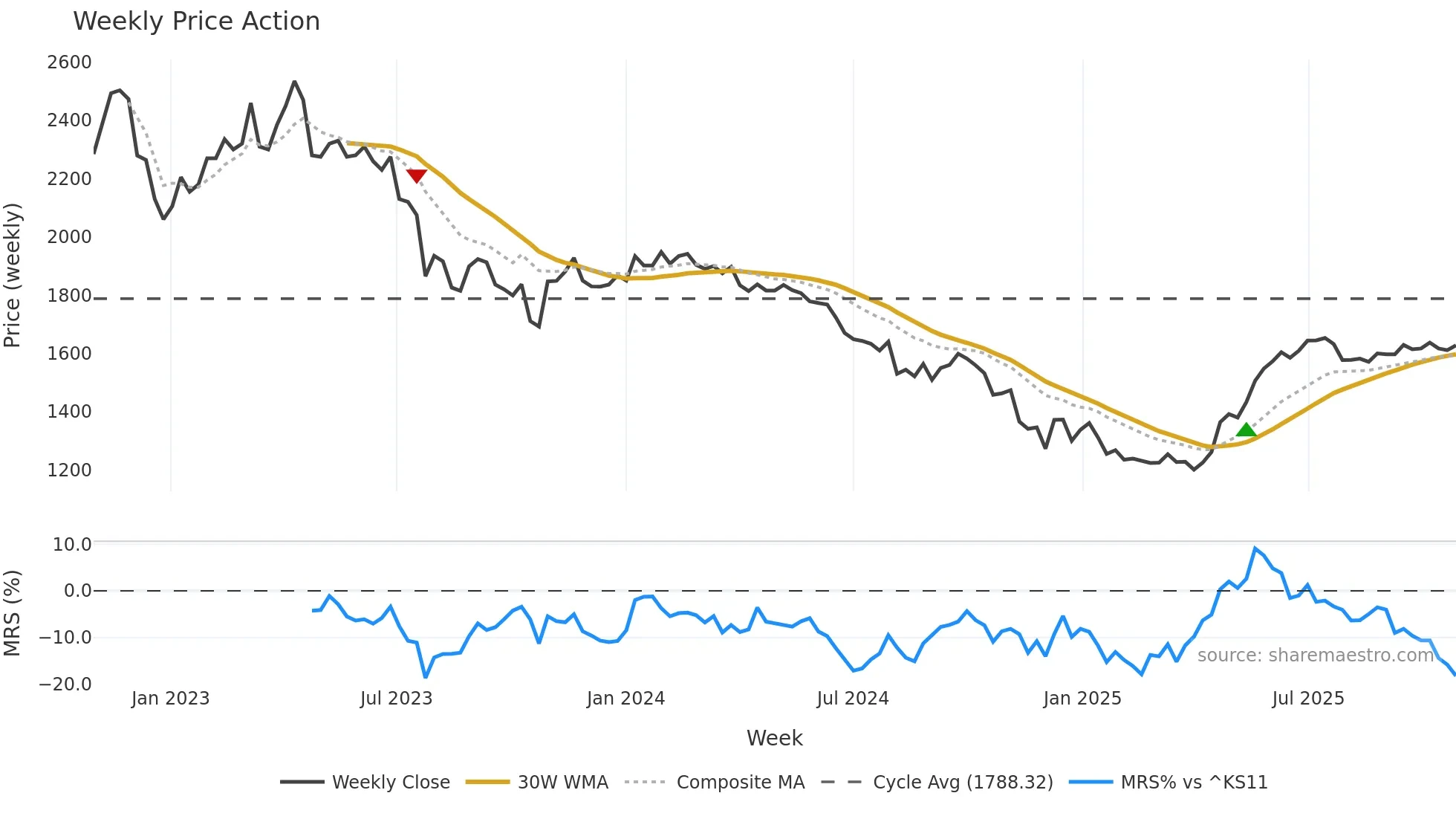

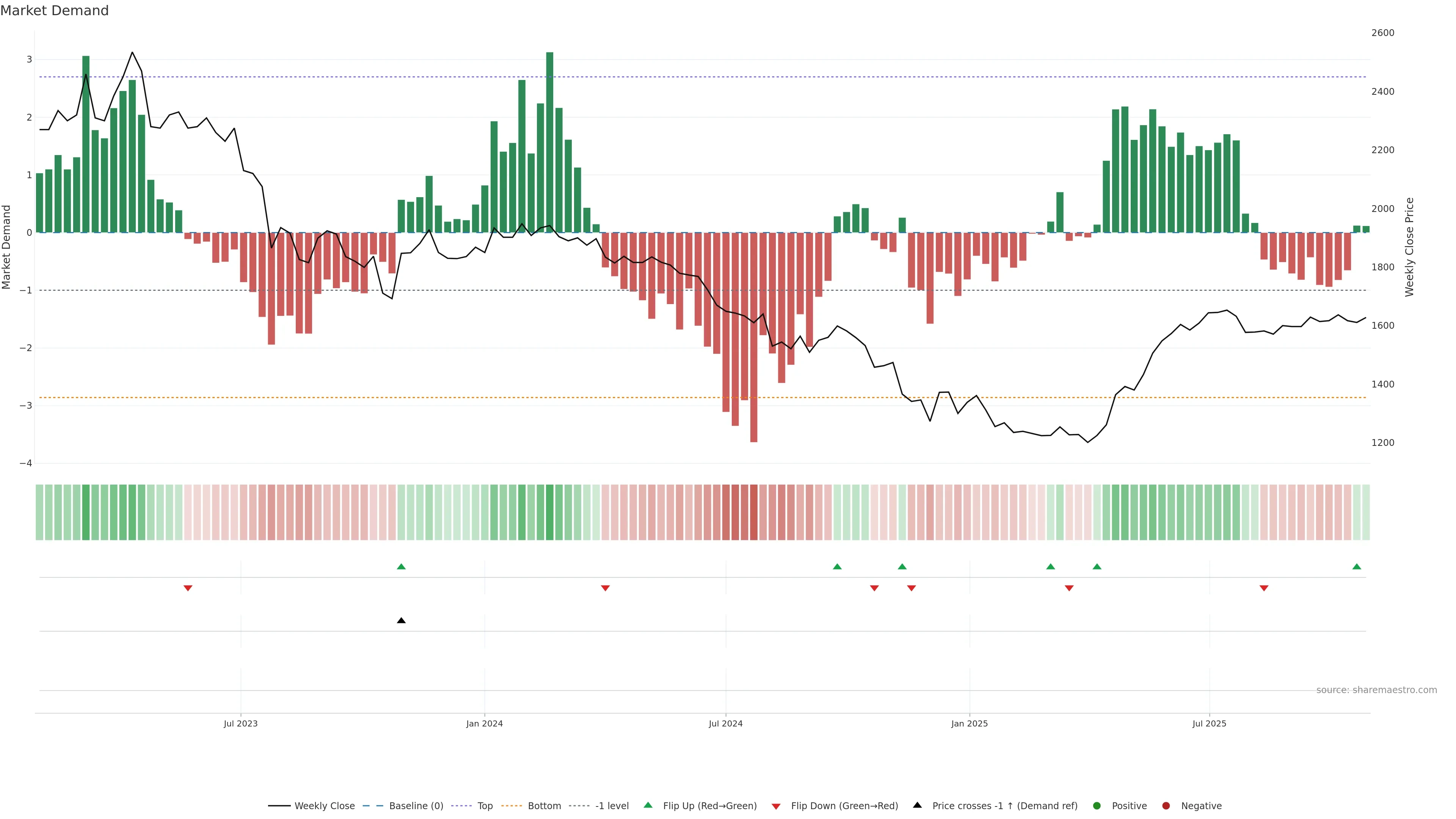

Bullish divergence: price made a lower low while Dynamics made a higher low.

Bullish divergence: price made a lower low while Dynamics made a higher low. Often an early tell for bottoming phases. In essence this reflects state changes, ribbon flips, and early trend anatomy with a bullish tilt.

pol 0.8

conf 0.65

strong · high

What it means

Bullish divergence: price made a lower low while Dynamics made a higher low. Often an early tell for bottoming phases. In essence this reflects state changes, ribbon flips, and early trend anatomy with a bullish tilt.

Implications

Improves odds for follow-through if pullbacks hold higher lows. (pol 0.80, conf 0.65 → strong/high)

Positive

Positive

pol 0.6

conf 0.402

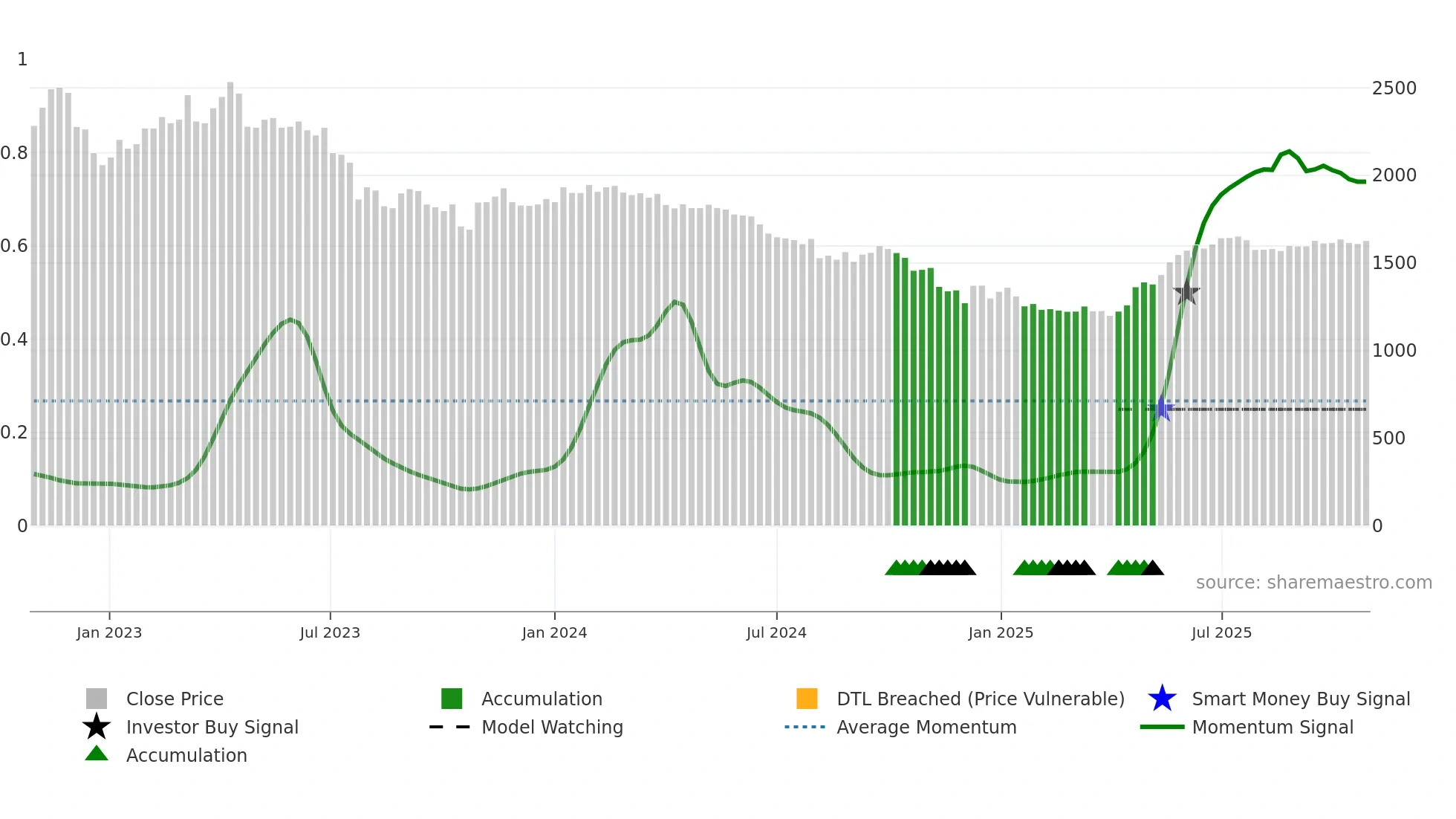

Dynamics turning up from negative territory.

Dynamics turning up from negative territory. Early trend repair often precedes price strength. In essence this reflects state changes, ribbon flips, and early trend anatomy with a bullish tilt.

Implications

Improves odds for follow-through if pullbacks hold higher lows. (pol 0.60, conf 0.40 → strong/medium)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}