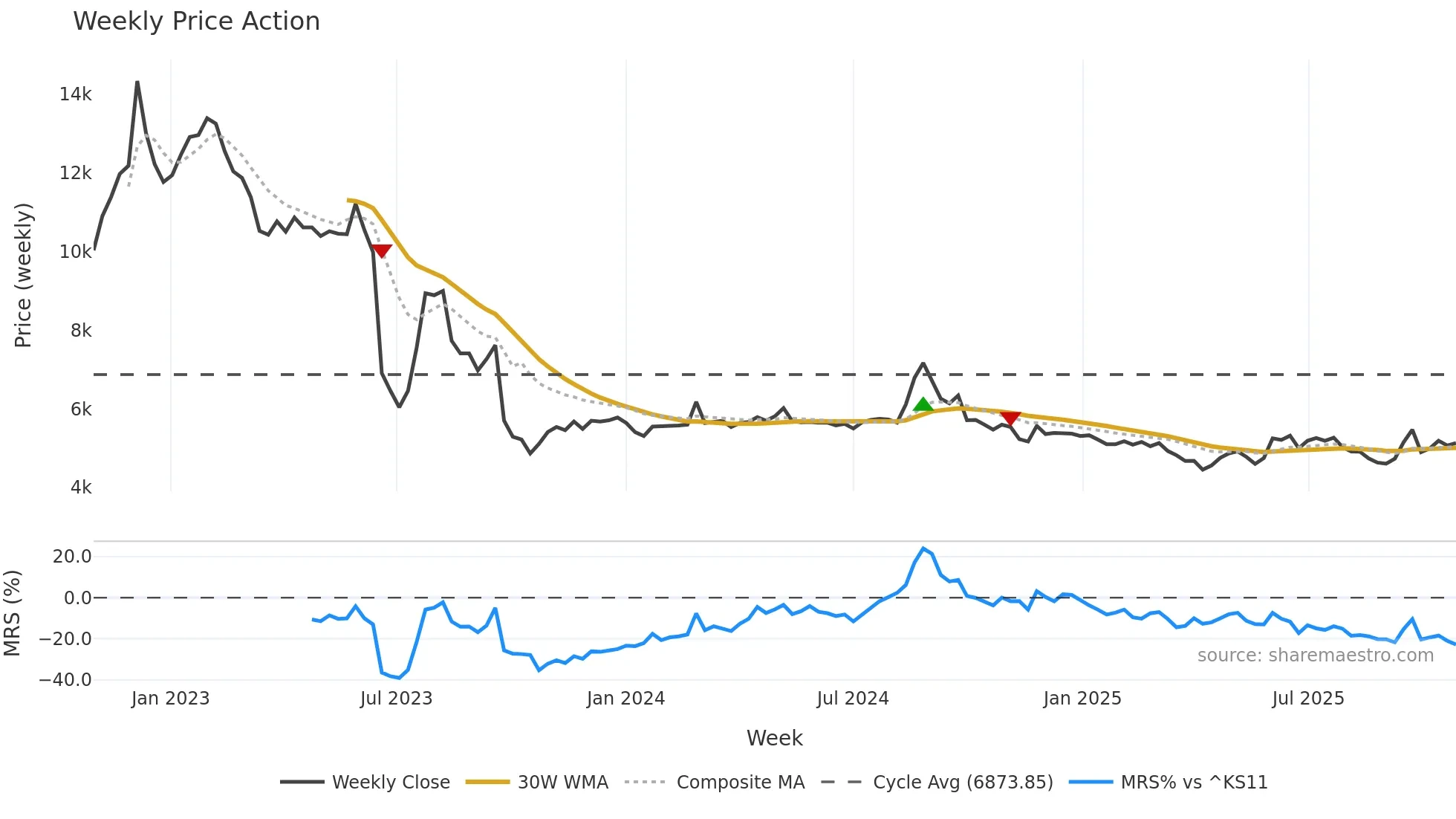

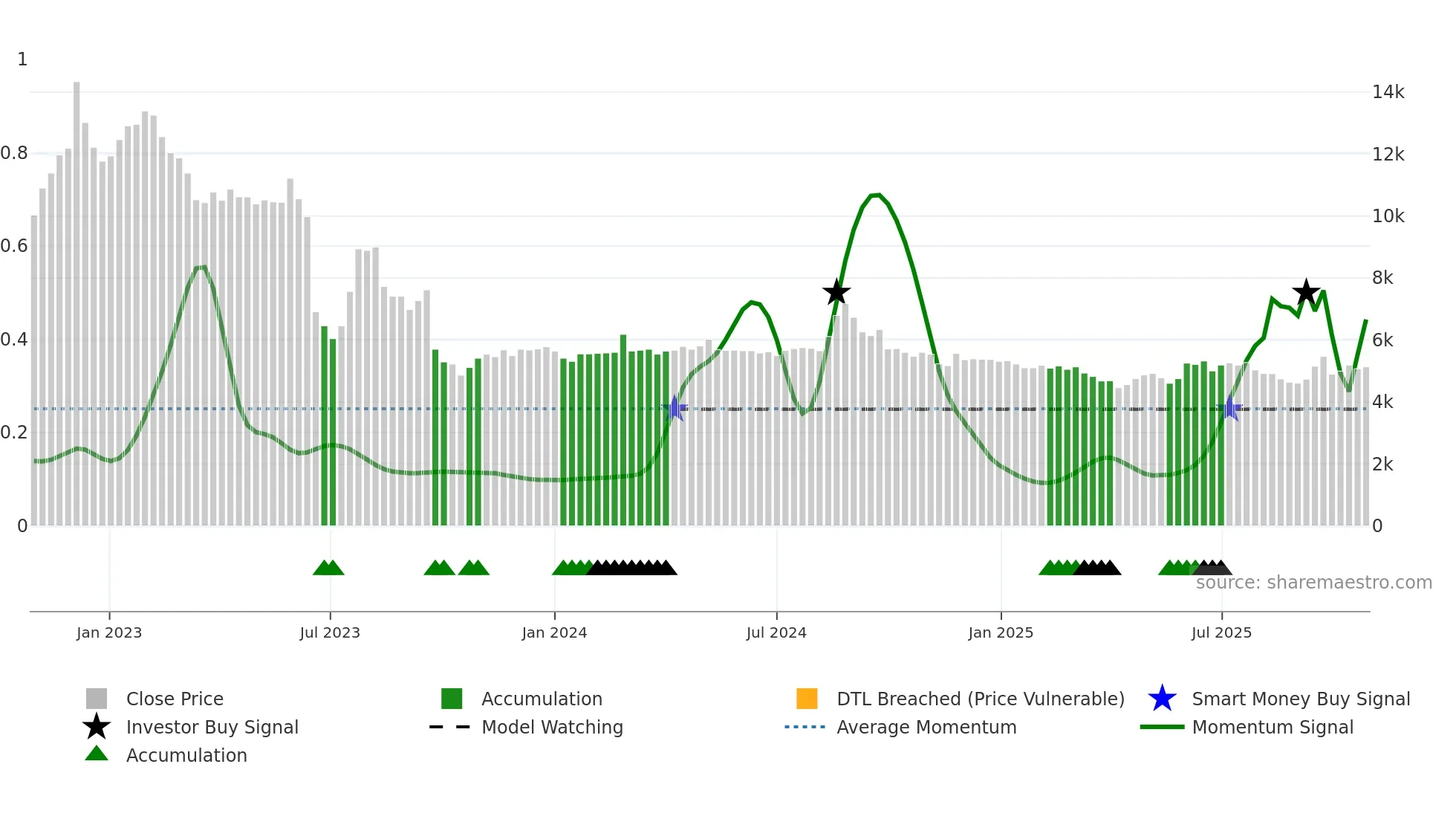

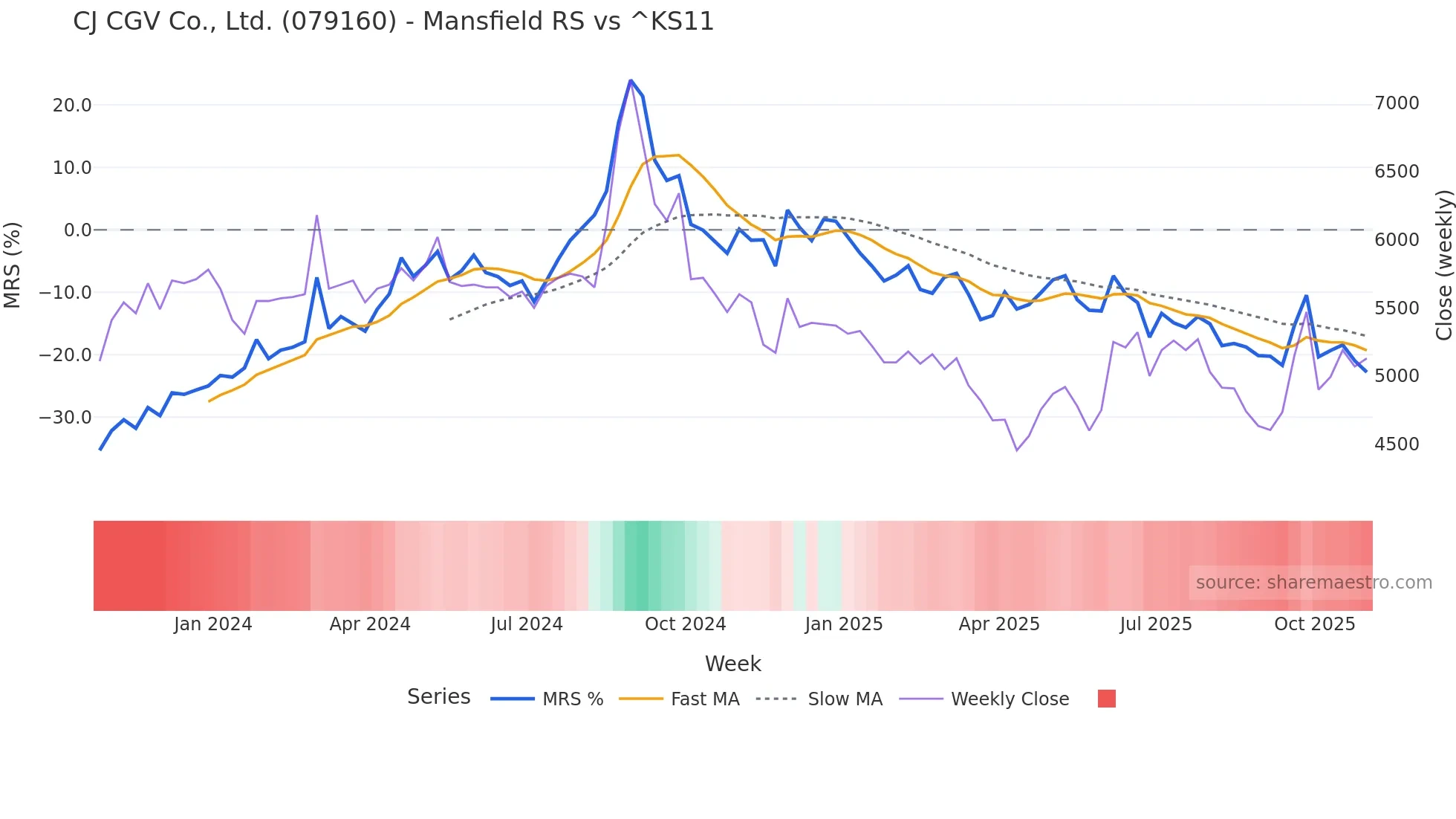

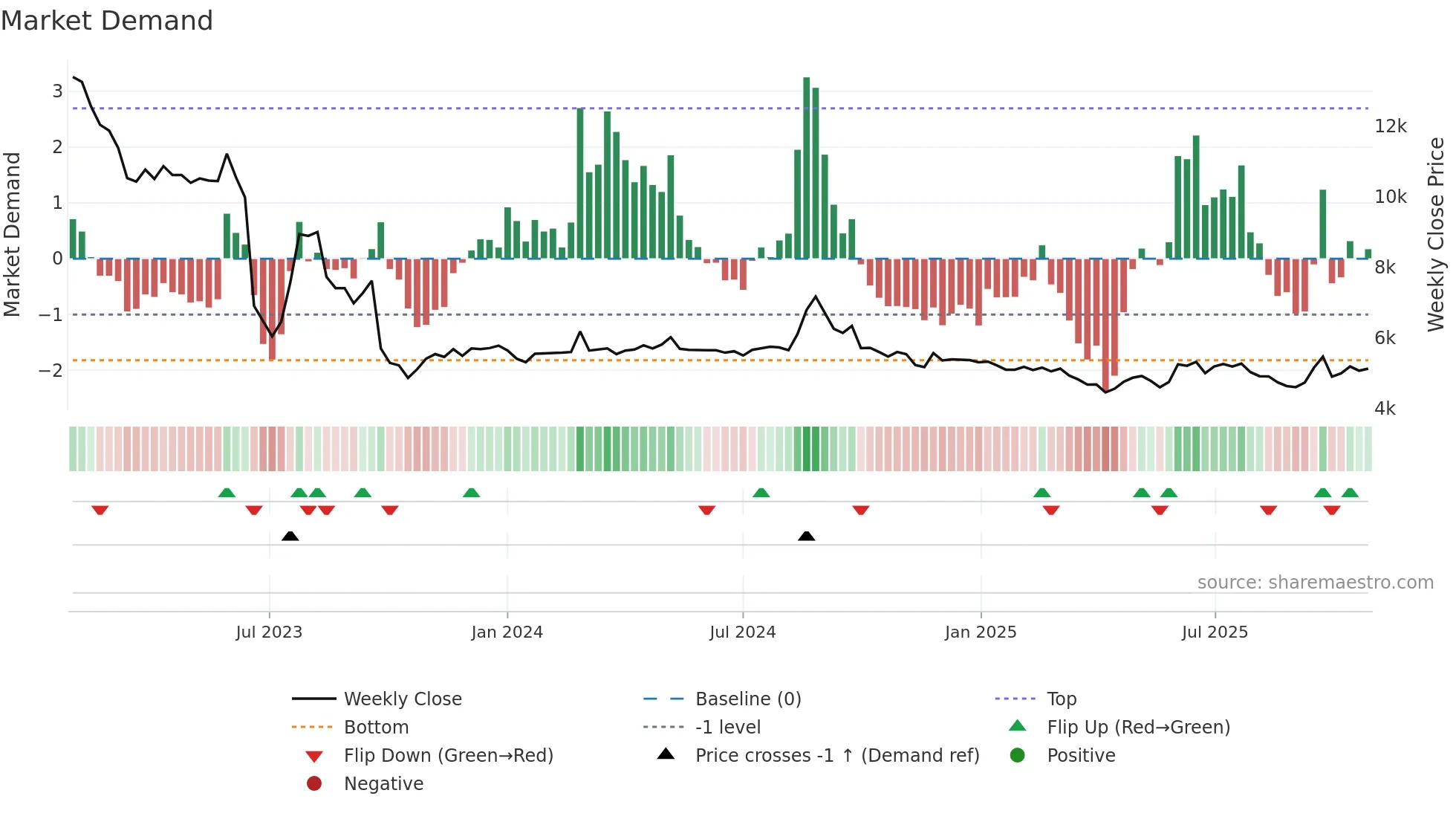

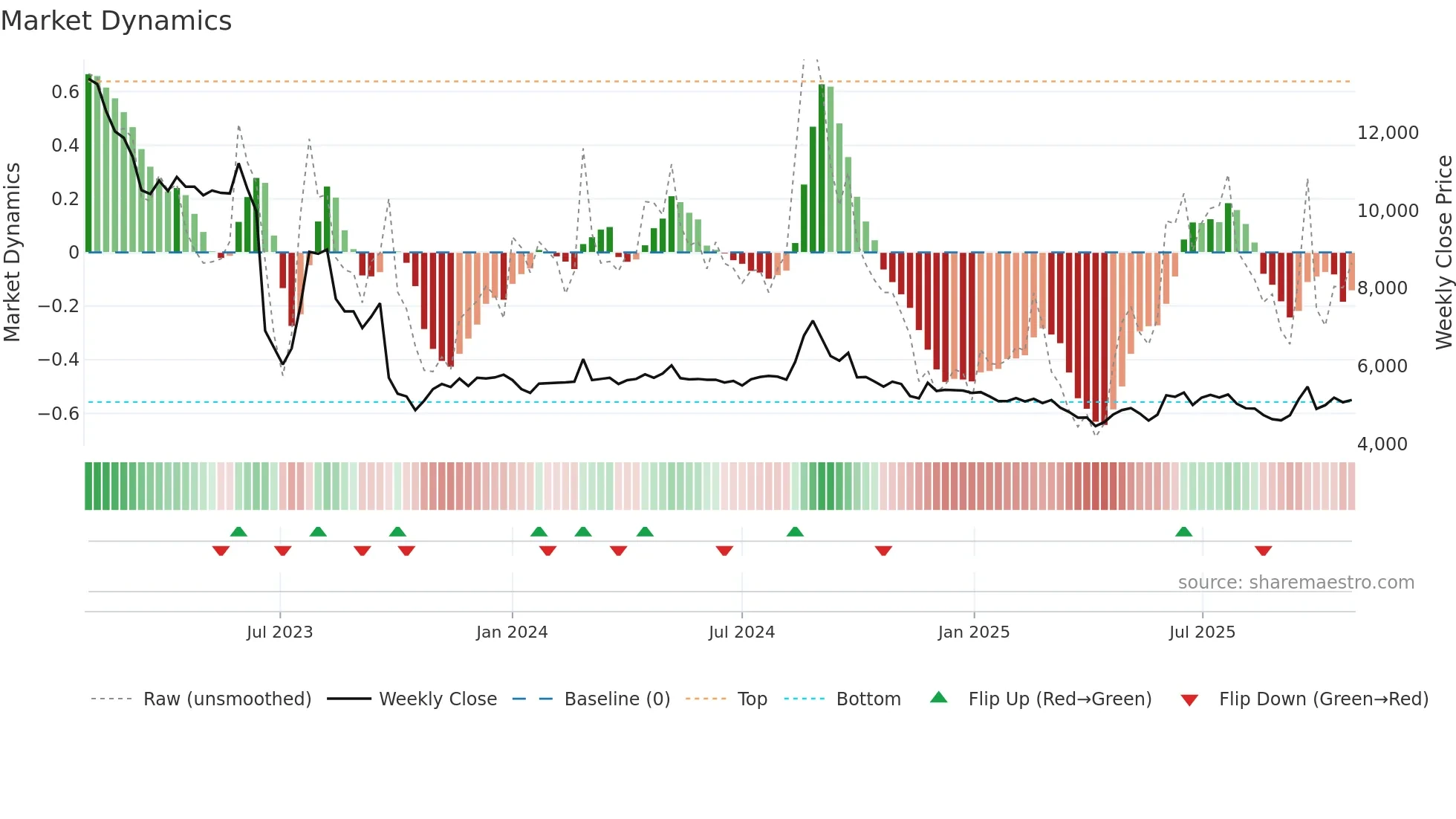

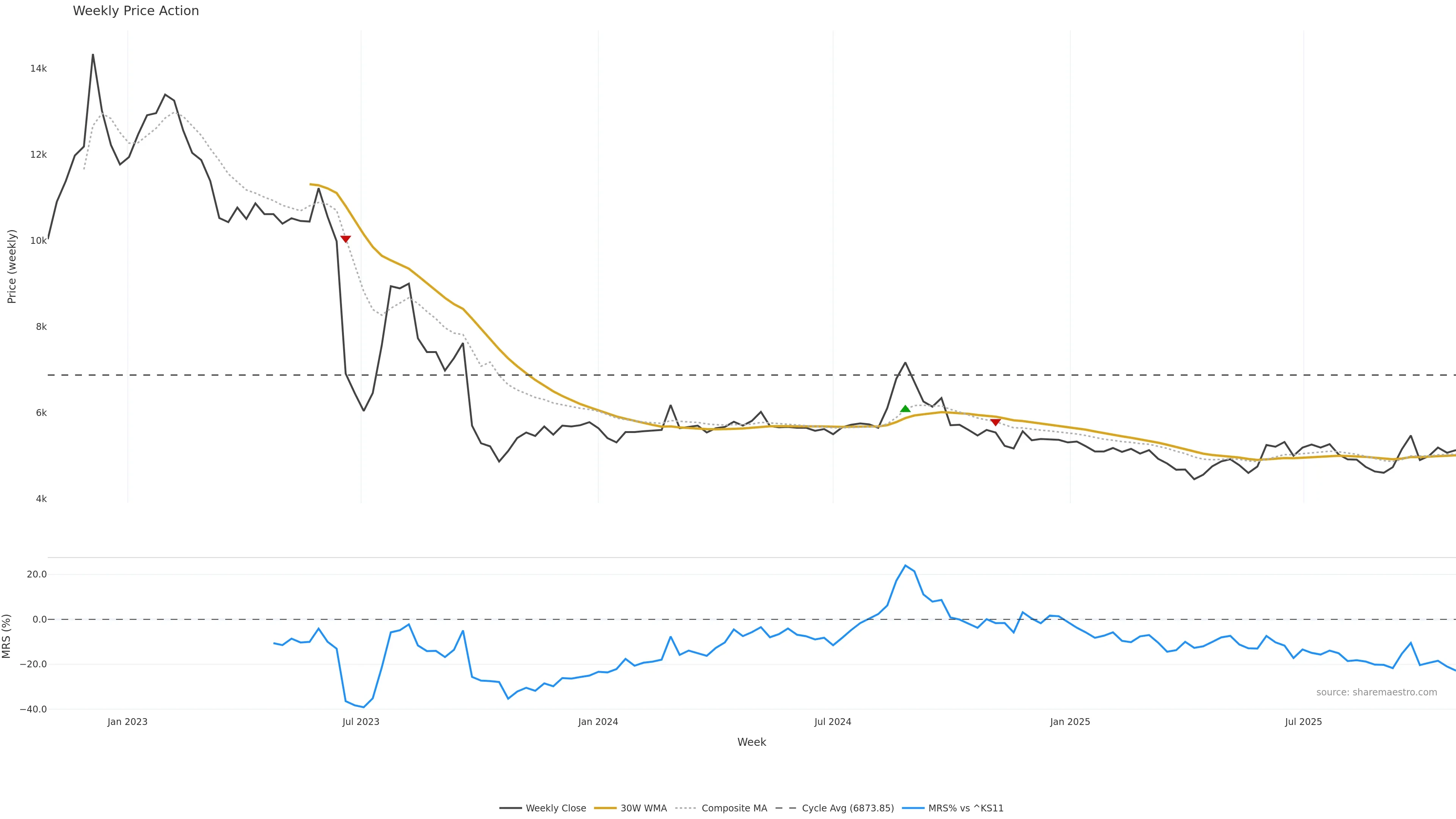

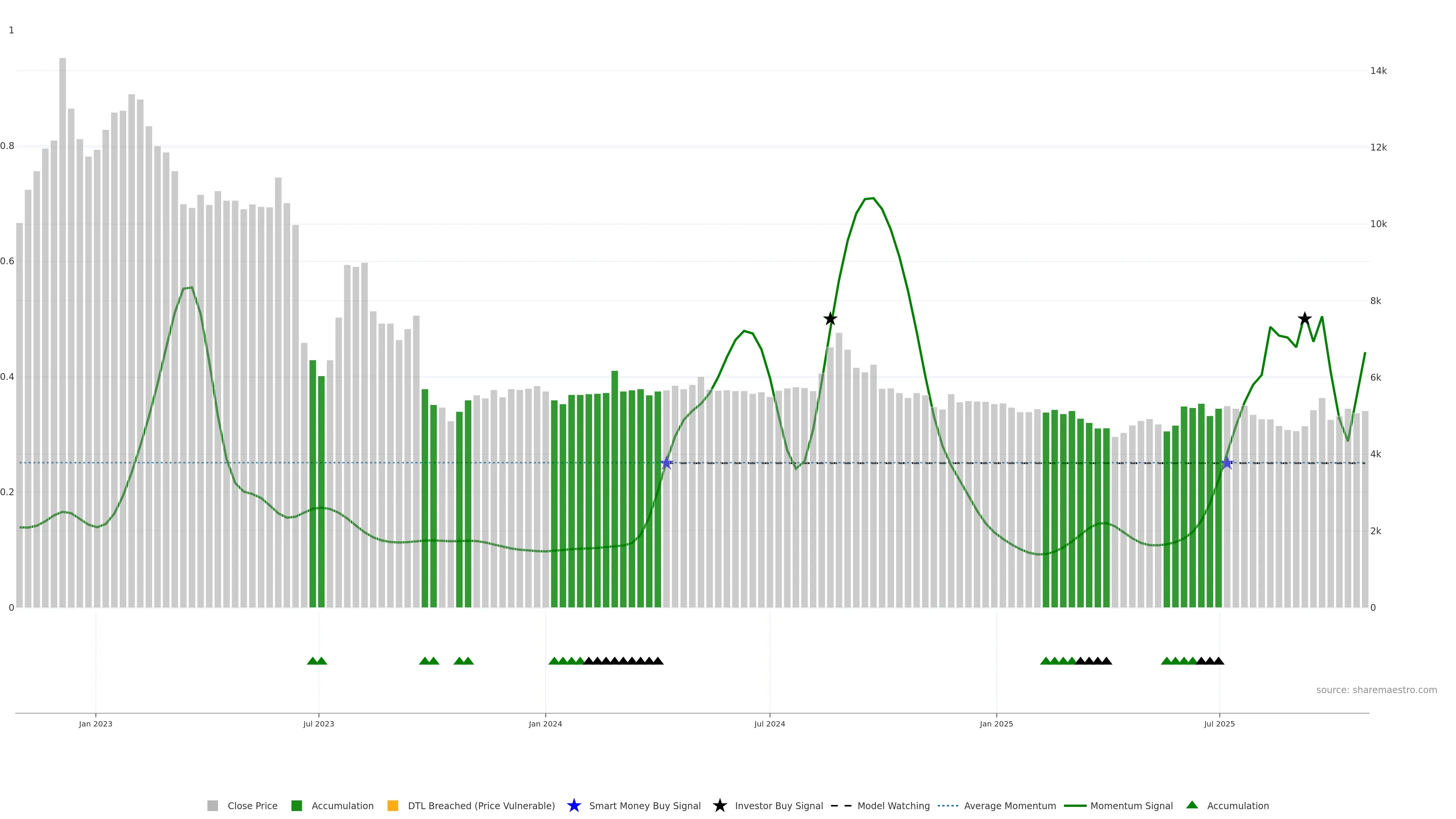

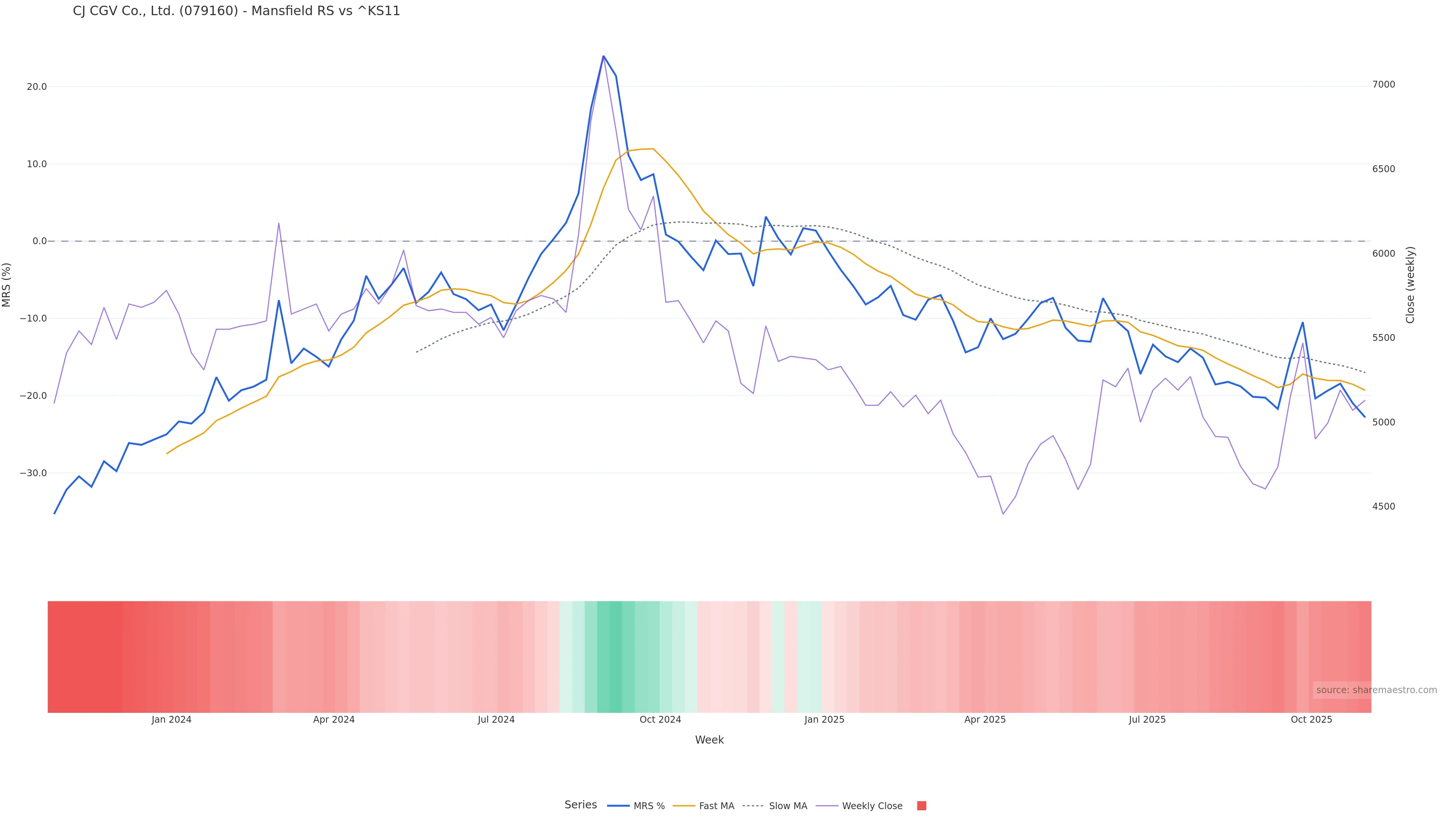

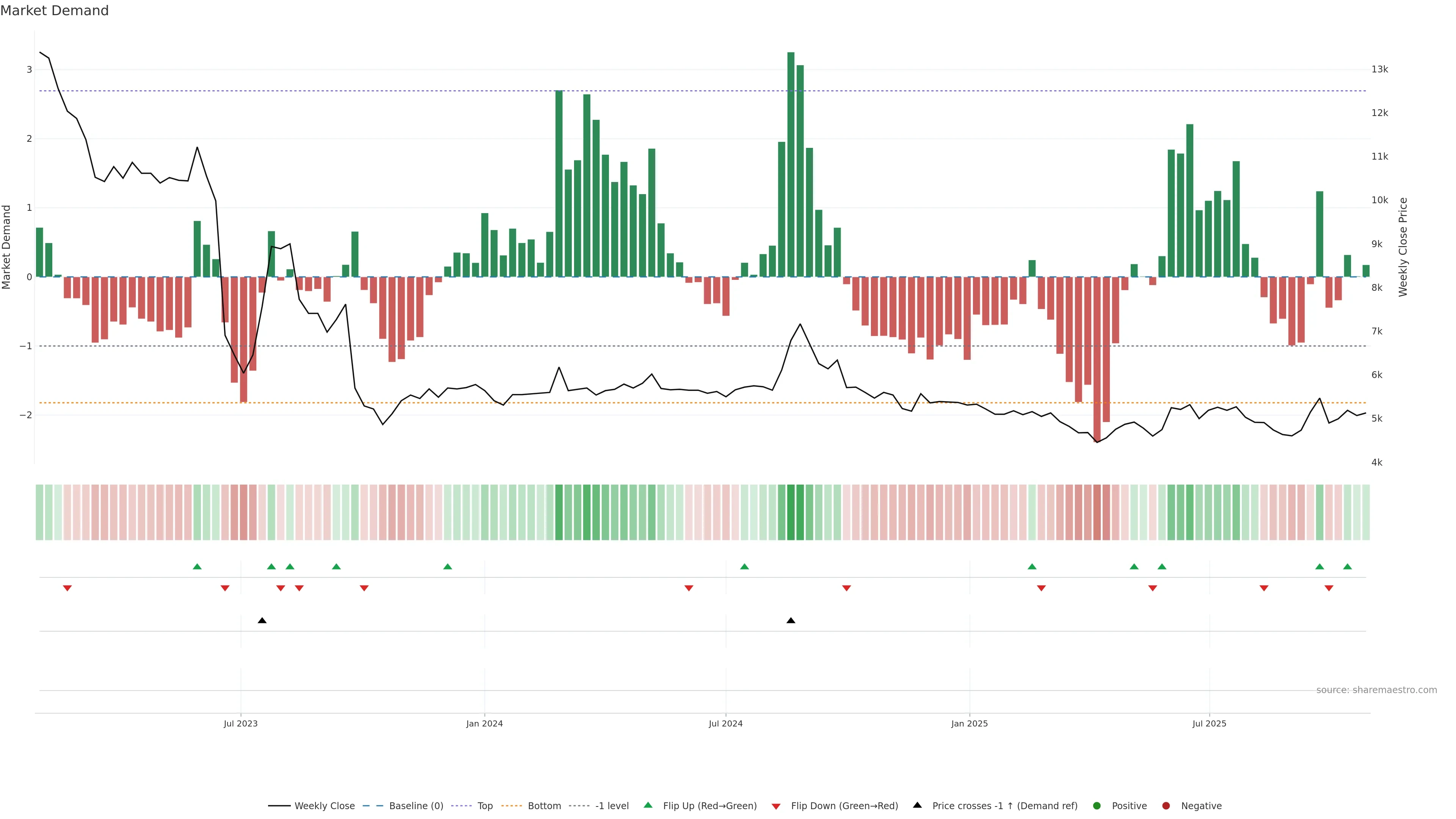

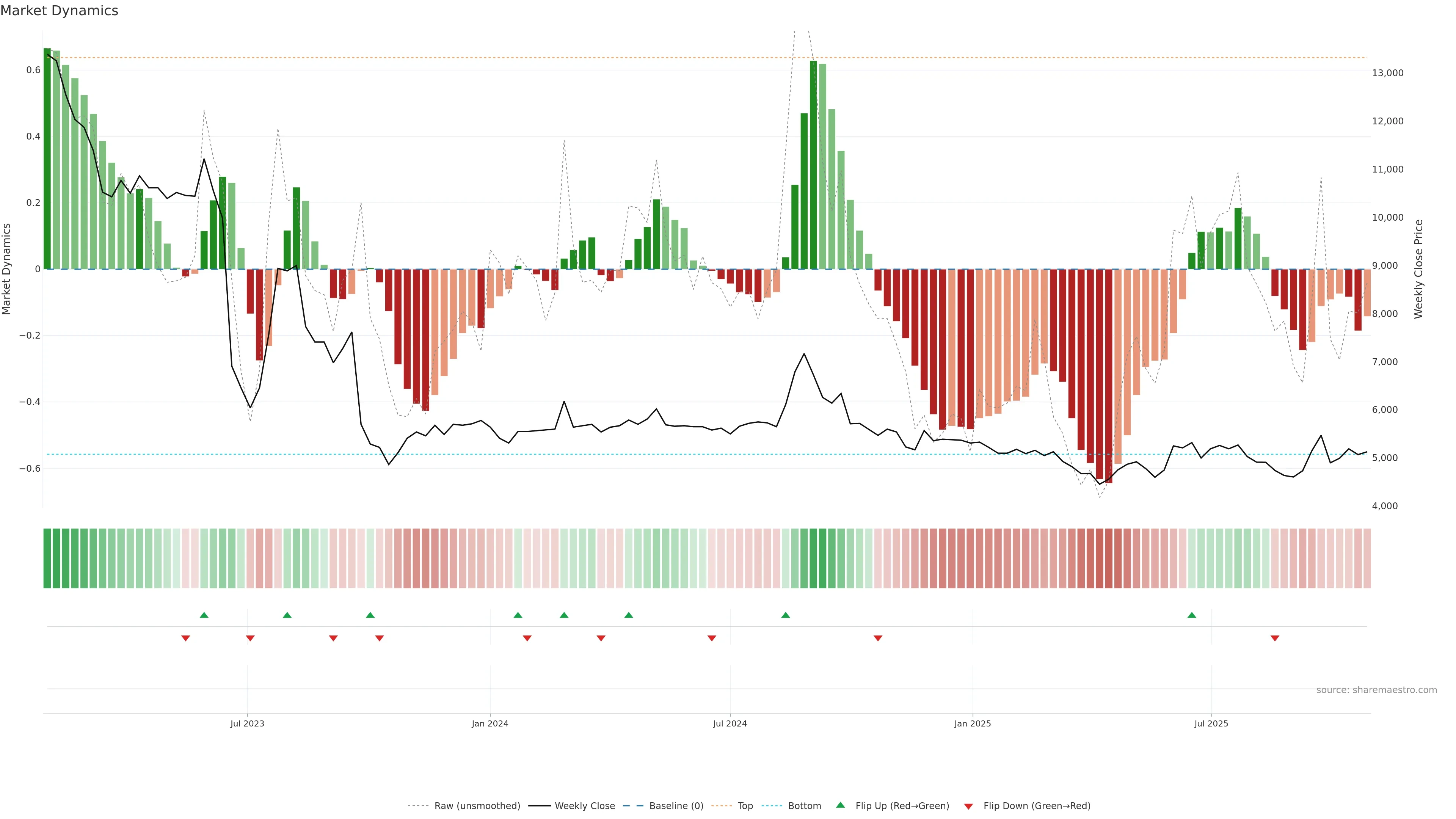

Market Dynamics

Dynamics turning up from negative territory. — Early trend repair often precedes price strength.

Score 0.6

+1 / -0

Level -0.142

Dynamics turning up from negative territory.

Dynamics turning up from negative territory. Early trend repair often precedes price strength. In essence this reflects state changes, ribbon flips, and early trend anatomy with a bullish tilt.

pol 0.6

conf 0.403

strong · medium

What it means

Dynamics turning up from negative territory. Early trend repair often precedes price strength. In essence this reflects state changes, ribbon flips, and early trend anatomy with a bullish tilt.

Implications

Improves odds for follow-through if pullbacks hold higher lows. (pol 0.60, conf 0.40 → strong/medium)

No additional observations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}